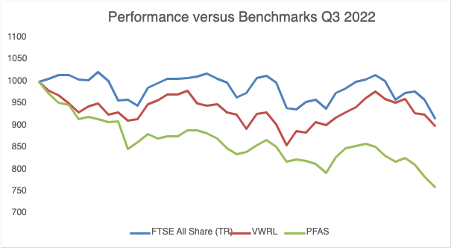

Performance versus Benchmarks

My portfolio was doing quite well this quarter until the past few weeks which has led to an overall quarterly decline of -7.31% and a YTD performance of -23.93%. It was also another quarter of underperforming my benchmarks; FTSE All share TR -3.9% Q3, -8.31% YTD and Vanguard World ETF (VWRL) +1.69% Q3, -9.97% YTD. The bright spot in 2022 has been the portfolio dividends which are currently running at 88% of the start of year forecast and with a large chunk of those dividends being on quarterly repeat, I am anticipating a comfortable beat against forecasts and possibly by as much as inflation. This is fortunate as our living expenses are drawn from dividend income.

To point the finger of underperformance at the portfolio’s overweight exposure to UK small and mid caps is all well and good but more recently, the ‘stable’ property and infrastructure funds have also fallen out of bed, thanks to rapidly rising gilt yields. Despite this reaction to UK fiscal and monetary policy, the underlying reality is that the US Dollar is crushing just about everything else this year with the dollar index (DXY) running hot at ~112.

I fear there is more pain still to come and yet, I remain optimistic and focused on my process. The plan from here is simple – to buy more of what I already own while value is on offer. The fly in the ointment is whether I will have sufficient liquidity to take full advantage.

Main Contributors and Detractors

| Q3 Top Contributors | Q3 Top Detractors |

| MEGP +18.7% | FDM -26.3% |

| FNX +9.5% | AAZ -23.9% |

| SPSY +8.5% | JIM -19% |

| MONY +6.4% | AEWU -17.9% |

| BSIF +5.7% | GAW -15.2% |

Q3 Portfolio Changes

| In | Out |

| Me Group International (MEGP) | Blackrock World Mining (BRWM) |

| CT Global Managed Income Trust (CMPI) | Henderson Far East Income (HFEL) |

| Henderson International Income (HINT) | Oxford Metrics (OMG) |

| Law Debenture Corporation (LWDB) | Jarvis Securities (JIM) |

| Alliance Trust (ATST) | Real Estate Credit Income (RECI) |

| Bioventix (BVXP) | Polar Capital (POLR) |

| FDM Group (FDM) | DSW Capital (DWS) |

| Record (REC) | |

| Schroder Real Estate Income (SREI) |

Still too much churn but there is mostly method in the madness. BRWM, HFEL and RECI all went because I felt they were becoming value traps but this meant giving up a fair amount of income as they were all 8% yielders (replaced by CMPI, HINT, LWDB and ATST). I also gave up a prospective 10% (uncovered) yield at POLR where I am uncomfortable about their short-term prospects (replaced by REC) and 7.5% at JIM where I decided to watch the FCA audit from the sidelines. Recent purchases include SREI which was bought in past few days of the quarter amidst the REIT sell-off and BVXP and FDM which were added to replace OMG and DSW early in September – the timing of the FDM purchase has proven to be particularly poor.

My star buy of the quarter has been Me Group International (MEGP) which has already paid out a chunky special dividend during the quarter while still offering up exceptional value – forecast top line growth of ~20%, alongside an ordinary dividend yield of ~8%.

Portfolio Metrics

| Weight | Average Yield | Average Volatility | Average Discount/Premium | Average Q/V/M | |

| Direct Equities | 53.00% | 5.07% | 3.14 | N/A | 89/42/66 |

| Funds (ITs/ETFs) | 46.83% | 5.93% | 1.63 | -13.84% | N/A |

The overall (weighted) dividend yield is 5.55% and weighted volatility has fallen to 2.45. All 3 QVM factors have risen, perhaps the most surprising being momentum which has risen from 54 to 66. The average discount on the fund segment has widened to 13.84% (cheap) with an average dividend yield of 5.93% (juicy).

If the portfolio were a single entity, it would now be a Balanced High Flyer (from Adventurous, Neutral).

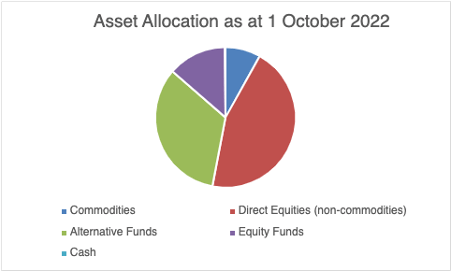

Current Asset Allocation

| Asset Allocation | % | # |

| Commodities | 8.09% | 2 |

| Direct Equities (non-commodities) | 44.90% | 12 |

| Alternative Funds | 33.39% | 11 |

| Equity Funds | 13.44% | 5 |

| Cash | 0.17% |

Notwithstanding some swap in/outs in the direct equity portfolio, my main focus this quarter has been reducing exposure to commodities which has facilitated an increased exposure to large cap equity funds.

Commentary

They say bear markets are where fortunes are made. I believe we are at the squeaky bum time of this bear market with capitulation now around the corner. As stated at the top of this article, it is a situation I would like to take full advantage of by buying more of the stocks and funds that I already hold, at lower valuations. This will require liquidity at the appropriate time.

Option 1 – Commodity and Resource Stocks

This bear market has helped me to refine my strategy (more on this in my year end update) and who I am as an investor. To that end, commodity/resource stocks do not fit with my long-term strategy as they are not compounders. This said, the two stocks I own; Anglo Asian Mining (AAZ) and I3 Energy (I3E) are both cash cows, reliable dividend payers and have exploration upside. They also provide exposure to commodities/resources that might prove lively as current macro events unfold.

Option 2 – Takeovers

The second avenue for creating some internal liquidity would be a takeover approach or two. When I look through my 12 non-commodity holdings, 8 are on single digit EV/EBITDA multiples and a further 3 are below 15. With the GBP/USD exchange rate close to all-time lows, I imagine several companies are vulnerable at current valuations. This said, I have only had one takeover this year (EMIS) which follows a three-year hiatus, so perhaps I am being optimistic with this scenario.

Option 3 – Failed Investment Theses

While I have a strong conviction in each of my holdings, there will always be occasions when my investment thesis fails. And when that happens, I sell. For example, Jarvis Securities (JIM) was axed in Q3 after announcing an FCA audit which created a material uncertainty.

Option 4 – Do Nothing

The final option I have is to do nothing. It is an unleveraged, long only portfolio and dividend income covers our living expenses. So, there is no compulsion to do anything at all.

I don’t know what the catalyst will be for a final major market sell-off but I think the macro storm clouds continue to suggest that something has to break.

- Inflation is still high

- Risk of recession is high

- Interest rates are rising and will likely need to continue rising to fight inflation

- Dollar strength continues to punish other asset classes and currencies

- Systemic risks are increasing (e.g. LDIs, Credit Suisse)

I have plenty of questions but very few answers. What will cause the dollar to weaken? A Fed pivot to avert systemic risk? An alternative reserve currency (e.g. BRICS)? China offloading its dollar reserves? And what of the UK? Are we a basket case or will funds flow back into UK assets?

Despite these macro factors, I remain convinced that the key to long term wealth is to own high quality assets and businesses with strong cashflows. I believe there is an abundance of these in my portfolio and I will be a happy chap to emerge from this bear market owning more of the same.

If nothing else, the final quarter of 2022 will be interesting.

Cheers

Simon (@BrilliantLeader on Twitter and Stockopedia)

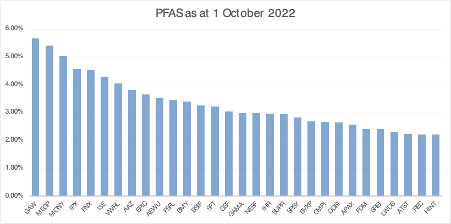

Disclosure – At the time of writing, my portfolio holdings and weightings are as per the following graphic