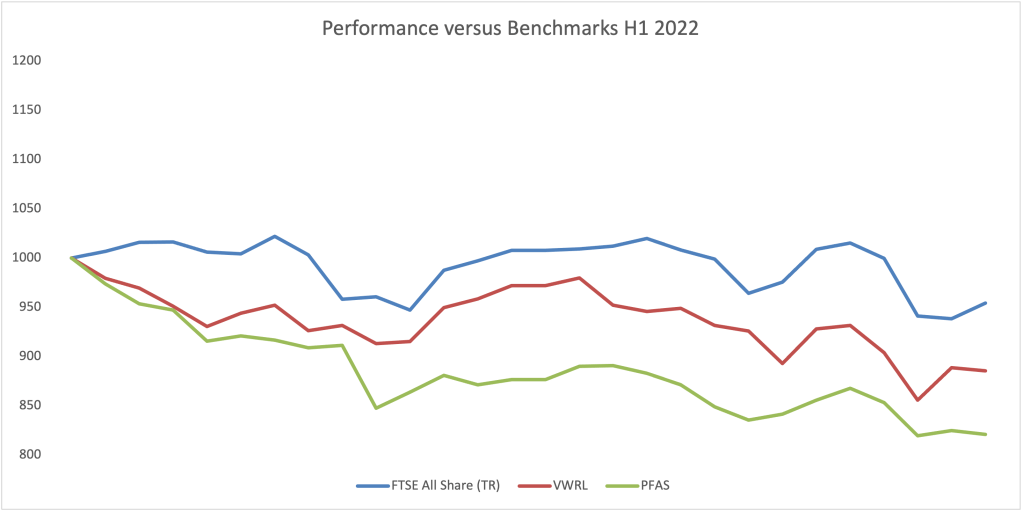

It continues to be a tough market environment. Most growth assets are now firmly in bear market territory and my portfolio (PFAS) has continued to suffer during the second quarter of 2022, falling a further 6.37% (-17.93% YTD) which was slightly better than the Vanguard World Equity ETF down 8.88% (-11.46% YTD) but slightly worse than the FTSE All Share TR Index down 5.33% (-4.59% YTD). [Note – I have had to discontinue tracking my third benchmark as Wikifolio made some inconvenient changes to their platform].

My relative underperformance versus benchmarks can be attributed to an overweight exposure to UK small and midcaps and latterly, the possible failure of the commodity trade (due to recession concerns) where I am also overweight.

On the positive side, dividend returns have exceeded expectations, achieving 52% of forecast at the halfway stage while traditionally being second half weighted.

Main Contributors and Detractors Q2

| Top 5 Contributors | Top 5 Detractors |

| EMIS +52% | IPX -40.8% |

| I3E +23.4% | BRWM -24.2% |

| FSFL +6.4% | GAMA -20.2% |

| SPT +6.4% | POLR -17.9% |

| NESF +6% | APAX – 15.8% |

A takeover offer for EMIS was the main highlight whereas some of the falls in the negative column have been brutal.

Portfolio Changes Q2

| Out | In |

| ARQQ | MONY |

| APF | BRWM |

| GDGB | SPSY |

| EAT | DSW |

| PCT | HFEL |

| EMIS | APAX |

| OMG |

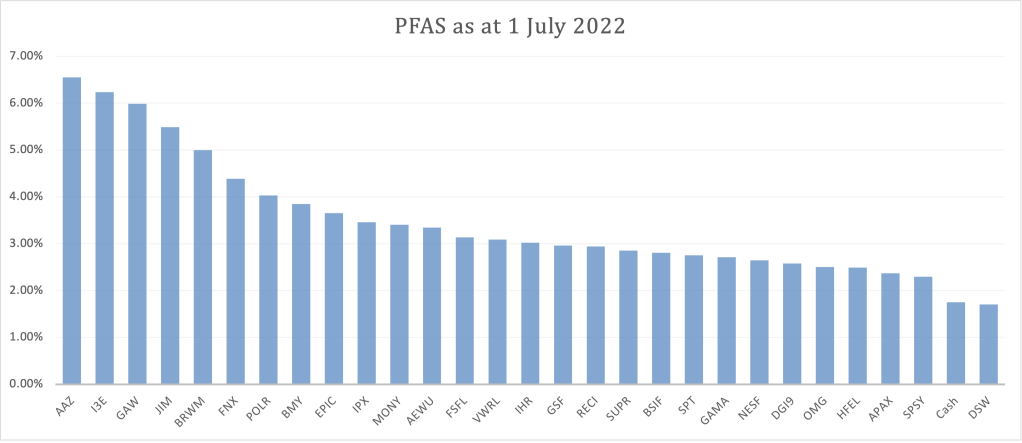

Therefore, total holdings have now risen from to 28 (from 27) made up of 14 funds (held mainly for income) and 14 direct equity holdings (held mainly for growth). Current holdings/weightings can be viewed here

Portfolio Metrics

Volatility has fallen (it’s all relative) to a weighted average of 2.51 while the portfolio’s natural yield has risen to 5.47% which seems like value territory to me. However, the Q/V/M averages have barely moved this quarter (I was expecting value to have risen but again, these rankings are all relative to the wider market). If it were a single stock, PFAS would currently have an Adventurous (Volatility) Neutral (StockRank Style) rating.

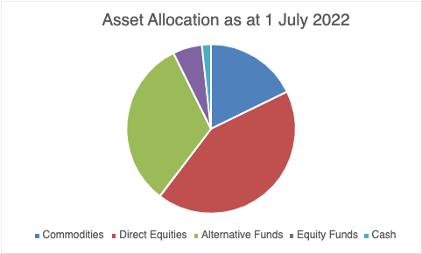

The breakdown between equities and funds can be seen here

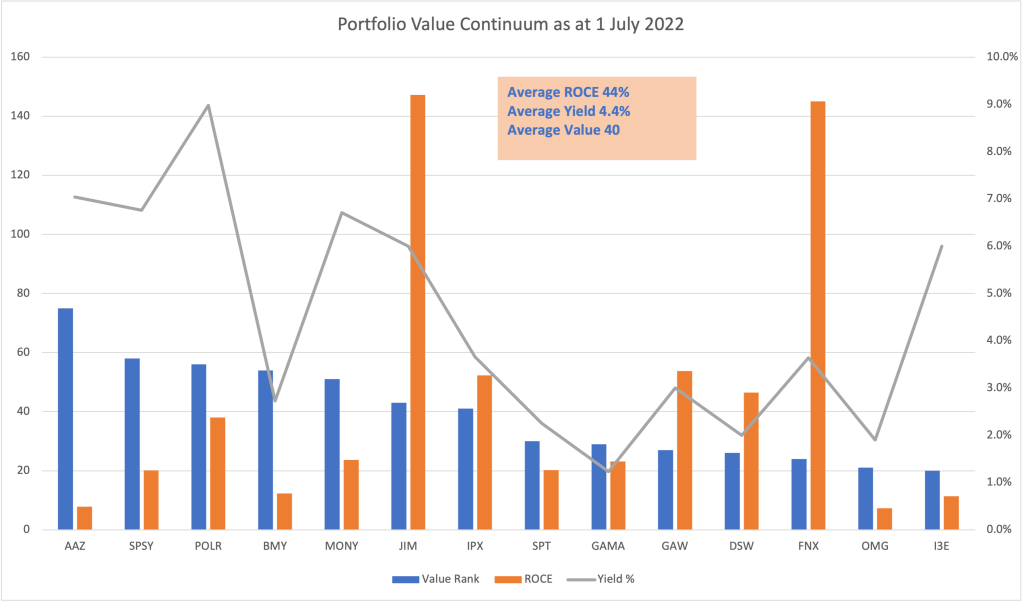

One of the charts I like to look at periodically is the Value Continuum for my direct equity holdings, overlayed with ROCE and Dividend Yield (see below). Average Value and ROCE are barely changed from when I last ran this chart six months ago while average dividend yield has risen by a full percentage point.

Current Asset Allocation

Commodities: 3 Holdings (17.78% weighting) – under active review, no watchlist candidates

Other Direct Equities: 12 Holdings (42.58% weighting) – two watchlist candidates

Non-Marked to Market Funds: 11 Holdings (32.31% weighting) – under review, one watchlist candidate

Large Cap Equity Funds: 2 Holdings (5.58% weighting) – six watchlist candidates

Commentary

My head feels as though it is going to explode following the macro environment this quarter. In summary, it seems as though inflationary fears have given way to recessionary fears (inflation + recession = stagflation). However, the recessionary fears seem to have been caused by the high inflation and commodities have sold off quite heavily, reducing inflationary fears. Meanwhile, the Fed continues to talk tough on inflation as the market looks for a sign it will pivot while in the UK at least, a summer of discontent looms with wage rise demands over 10% becoming the norm. Dollar strength (the dollar index sits at around 105) is hurting just about everyone else, including the UK where cable sits at around 1.20. In the background the BRICS (Brazil, Russia, India, China and South Africa) countries along with Argentina and Iran are planning to launch their own reserve currency/asset to reduce dependence on the US dollar. That bloc account for around 45% of the world’s commodity and energy production. How long before they start trading these commodities in their new currency? That Silk Curtain is being drawn.

How do you position a portfolio for that set of circumstances? Cash seems like an eminently sensible strategy – more so if someone would be kind enough to ring the bell at the market bottom!

For my part, I remain fully invested and continue to follow my process. Putting aside commodity holdings, I own a dozen, high quality UK small/midcaps which I plan to hold for as long as management continue to execute on their strategy. They all have strong balance sheets, pay dividends, have a runway for growth and resilient business models. I have two other companies I would like to add to this focused portfolio, should the opportunity arise.

The alternative asset funds have generally performed unspectacularly well with low volatility, reliable dividends and rising NAVs. However, valuations have recently started to come under some pressure and broker downgrades have started appearing. I am considering reducing weight to this portfolio segment but am not in any immediate rush to do so.

An 18% commodity weighting is focused on just three holdings – AAZ, I3E and BRWM. The two direct equity holdings carry their own idiosyncratic risk and opportunity while the Blackrock World Mining trust provides diversified large cap exposure. I am currently watching very closely to see if the commodity thesis will fail, at least in the short-term. To that end I will be deciding during Q3 whether to stick, twist or fold with this asset allocation. My most likely course will be to reduce AAZ and I3E (both have been top sliced in Q2) while BRWM is more likely to be held for the longer term.

The obvious gap in my portfolio is large cap equity exposure which currently comes via just two holdings; VWRL and HFEL. I currently have six investment trusts under consideration to fill this void and I plan to buy at least two of them during the third quarter.

It has been three years since I last had a takeover in the portfolio, so imagine my surprise and delight when EMIS received a take over bid for a 46% premium (around the same price as my three year price target, so a big win on opportunity/time). When I look at current valuations, I wonder if any other holdings will succumb to takeover approaches, especially from larger US rivals? In the meantime, my main focus in July will be picking through trading updates and outlook/results announcements. I am expecting a raft of broker downgrades across the piste but am hopeful that my holdings will avoid the worst of it.

Bear markets are tough when you are going through them but when you look back with hindsight, they were an opportunity. Some bear markets are over very quickly (e.g. March 2020) but others grind on for longer. This current market feels much like the aftermath of the Dotcom crash which ran from 2000-2003. It was a long hard slog. Good news was sold. Bad news was punished. Large cap value eventually led the market out of that bear market but it was a long time coming. Once I have added some of that asset class to my portfolio, I plan to hunker down and focus on dividend income until this phase of the bear market passes.

Enjoy the summer folks!

Simon @BrilliantLeader on Twitter and Stockopedia

Disclosure – At the time of writing, my portfolio holdings are as per the graphic below: