There is no getting away from the fact that 2022 was a pretty ugly year for most investors. Most asset classes and stock indices have under-performed, especially in real terms given this inflationary environment we are currently living through. Dollar strength has been the main protagonist with Russia’s invasion of Ukraine and China’s continued Covid lockdowns providing a triple headwind for markets. In the UK, we also had to contend with the bizarre political shenanigans of a divided governing party, including the poorly timed policies of the, blessedly brief, Truss/Kwarteng era.

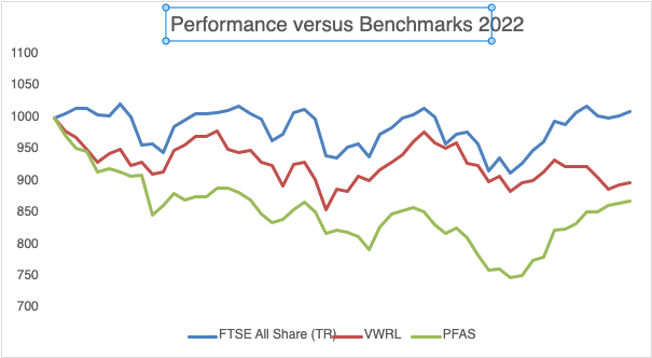

Performance versus Benchmarks

My own portfolio has not been immune from this market turmoil, especially given its overweight exposure to UK mid and small caps. Despite a run of ten consecutive positive weeks and a 14% quarterly gain to end the year, the final tally is a capital loss of 13.07% versus my benchmarks; the FTSE All Share TR gaining 1.14% and the Vanguard World ETF (VWRL) losing 10.22%.

The main bright spot for the portfolio throughout 2022 was an increase of 12.5% in dividend income. I am also extremely satisfied with my CAGR of 21% since portfolio inception (2016) which has now been through Brexit, Covid and the 2022 Bear Market. The full performance analysis can be viewed here.

Main Contributors and Detractors

There were some big winners in the fourth quarter; Games Workshop (+47%), Argentex (+38%), Impax Asset Management (+37%), Me International (+35%), Record (+33%), Fonix Mobile (+30%), Bloomsbury Publishing (+22%). In fact, all of the stocks and funds I currently hold are in positive territory for the quarter as the detractors have all been sold (see below). Moreover, all bar one of my holdings is currently in profit – the sole losing position being Gamma Communications.

The Pivot

As I mentioned recently when I was a guest on the Twin Petes Investing Podcast, I have exited all of the renewable energy and infrastructure trusts and all bar one of the REITs held at the start of Q4. And as per the signpost on this blog at the end of Q3, I have also exited all of my commodity and resource holdings (except for Blackrock World Mining Trust) as these are no longer consistent with my strategy (see below). This provided the liquidity to buy more of virtually all existing holdings and most of my primary watchlist of UK listed mid and small cap companies, two of which; K3 Capital and Crestchic, have already been sold in the market following takeover activity.

It has been a liberating process!

Strategy

The best learning tends to take place during a bear market and in my case, this has been to refocus on who I am as an investor and to refine the strategy I will be pursuing going forward. I have captured this in full on an updated Investment Strategy page and you will also note I have changed the portfolio name to Compound Growth & Income (CGI) to better reflect this renewed strategy. It is not an entirely new approach but it is one I had drifted away from, firstly post Covid and subsequently adapting to Macro events.

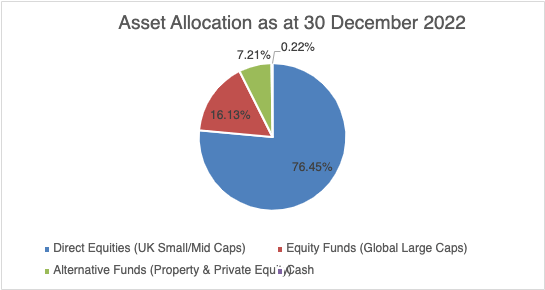

Current Asset Allocation

There are currently 26 holdings in the portfolio; 6 funds and 20 direct equity holdings. The direct equity holdings are all UK listed mid and small cap companies and therefore, the funds give me exposure to other asset classes, mainly large cap equities (UK and Global).

This means that it is a portfolio with plenty of home bias and a high dependency on funds flowing into UK mid and small caps as an asset class. That is deliberate and comes with its own risks. Within the asset class, I am confident I own a diversified bunch of high-quality companies that should do well on a one-, three- and five-year view. As ever, my thesis for each will be tested each time there is news to digest.

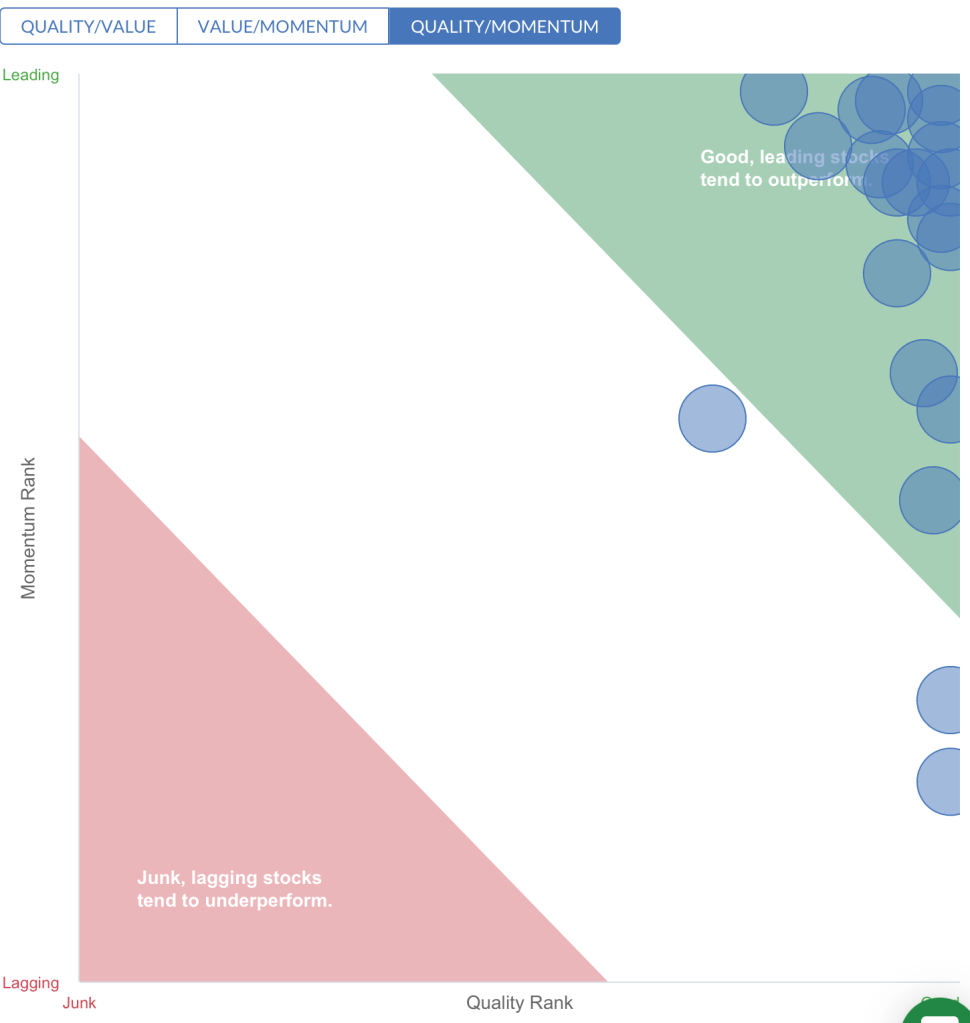

And lest anyone should accuse me of style drift…

…it has been quite a while since I have seen this set up across the portfolio.

QARP Checklist

One of the most productive aspects of the year has been to develop and refine my QARP Checklist. This enables me to efficiently assess companies for their key quality characteristics and whether there is an opportunity to buy them at a reasonable price. This 12-point checklist also provides a framework by which to assess the progress being made by companies that I already own. I should emphasise that this is not the only screen that I use (I have 8 currently) and neither is it a 100% pass/fail but if a company falls short against this checklist, then I want to understand where it falls short and whether I can live with that shortfall based on my additional company research.

Of the 20 companies that I currently own, 7 of them pass all 12 (these are GAMA, MONY, FDM, FSG, MEGP, REC, AGFX) and if I relax the PEG criterion a further 2 companies (SPT and SPSY) enter the fray. When viewed across the whole portfolio, the averages are very strong, as per the table below:

| QARP Checklist | Pass Rate | Average |

| ROCE % (5 Yr Avg) | 15% | 36.90% |

| ROE % (5 Yr Avg) | 15% | 36.55% |

| CROIC % (Last Year) | 15% | 60.10% |

| Gross Margin % (5 Yr Avg) | 20% | 57.30% |

| Operating Margin % (5 Yr Avg) | 10% | 22.55% |

| Net Gearing % (Latest) | 30% | -49.26% |

| P/OCF (TTM) | 20 | 17.76 |

| PEG (TTM) | 2 | 1.82 |

| EV/EBITDA (TTM) | 20 | 10.96 |

| Earnings Yield % (TTM) | 5% | 8.80% |

| Dividend Yield % (TTM) | 1% | 3.56% |

| EPS Growth % (1 Yr Forecast) | 5% | 23.30% |

| Checklist Passes n/12 | 10 |

Would you be interested in owning a company that boasted those average metrics?

Reasons to be Cheerful

I shall leave you with five reasons why I am optimistic going into 2023 (and for balance, I have also provided the pessimistic version).

1. My portfolio has momentum (I should have sold the bounce).

2. Inflation might have peaked (it is still high).

3. The recession might not be as deep or as long as feared, especially given high levels of employment (employment is a lagging indicator and the RNS airwaves will be littered with profit warnings and downgrades).

4. Bear markets are inevitably followed by bull markets (yes, but when?).

5. The Fed and other central banks will pivot and this will be the start of the next bull market (The Fed won’t pivot until either inflation is tamed or a systemic risk emerges by which time the economy will be broken).

Are you glass half full or empty?

I wish all my readers and followers a happy, healthy and prosperous New Year and please feel free to chat with me on Twitter or Stockopedia where I go by the handle @BrilliantLeader.

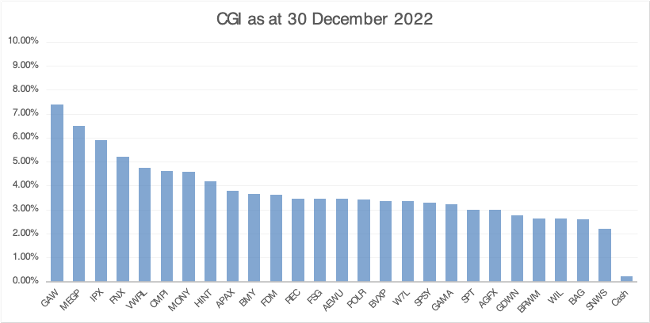

Disclosure – At the time of writing, I own all of the companies listed in the graphic below or if you are reading this in the future, my latest portfolio holdings can be viewed here.