Welcome to my Q3 portfolio review, reflecting on a quarter that has seen positive progress along with the addition of several new holdings which have expanded my portfolio (PFAS) to maximum size (based on my self-imposed limits) of 32 holdings (16 Direct Equity holdings and 16 Investment Companies).

Chugging Along (with a wobble at the end)

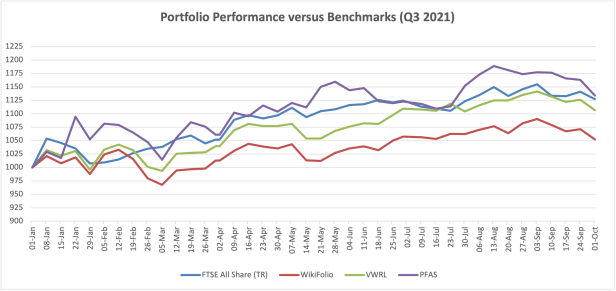

For the most part it was a successful quarter with steady gains in both July and August. However, things drifted in September with a more significant wobble in the final week of the quarter. Generally, these moves are not stock specific and my take is that it is a reflection of the market moving into risk-off mode and from growth to value (again). In that context, I am satisfied to have (marginally) outperformed all three benchmarks once again and to have achieved a positive return for the quarter, moving my year-to-date to +13%.

Performance versus Benchmarks

Contributors and Detractors

| Top 5 Contributors Q3 | Top 5 Detractors Q3 |

| Arqit Quantum (+85%) | Games Workshop (-10%) |

| Jarvis Securities (+20%) | Gamma Communications (-8%) |

| EMIS (+19%) | Polar Capital (-7%) |

| Spirent Communications (+10%) | Anglo Asian Mining (-5%) |

| EKF Diagnostics (+9%) | Spectra Systems (-3%) |

The portfolio continues to ebb and flow with EKF coming from last quarter’s naughty step into the top contributors list and three of last quarter’s stars detracting from this quarter’s performance (GAW, GAMA and POLR). The anomaly this quarter is Arqit Quantum (ARQQ) which was only added to the portfolio in the middle of August (via a SPAC) ahead of what has so far proved a successful, albeit volatile IPO (or despaccing to use the correct lingo). So far, the company has barely delivered any news or further evidence of commercial progress – hopefully that will change in Q4 and the share price will settle down a bit. Beyond that, some healthy contributions from steady-eddies JIM, EMIS and SPT, all in response to positive business performance and outlook statements.

Portfolio Changes

From the outside looking in, the changes this quarter might have looked a little chaotic but mainly, the changes were part of a plan to expand the portfolio, diversify income and provide a better balance between risk-on/risk-off market conditions. I also took the opportunity to whittle the direct equity holdings down to my 16 highest conviction stocks. If I were 10 years younger and in capital appreciation mode, these 16 small/midcap holdings would be my entire portfolio. But I am retired and in capital preservation mode with the main aim now being one of ensuring that both my capital and income remain ahead of inflation. And to that end, I have spent much of this year researching and adding investment companies to the portfolio, a process that I finalised this quarter. I will write more about this portfolio structure and how I have approached diversification, especially in relation to the core dividend income, in a future blog article.

As part of the process of facilitating these changes, I halved my position in largest holding, Anglo Asian Mining. For a couple of years now I have been carrying an overweight position in this stock and while I still have confidence in the company, the concentration risk was something that I wanted to reduce.

Other portfolio changes during the quarter were as follows:

| Exits | New Holdings | In/Out |

| Polymetal International (POLY) | Ediston Property (EPIC) | BMO Managed Portfolio (BMPG) |

| Henderson Far East Income (HFEL) | Record (REC) | Tate & Lyle (TATE) |

| Personal Group (PGH) | Arqit Quantum (ARQQ) | Secure Trust Bank (STB) |

| Smart Metering Systems (SMS0 | Apax Global Alpha (APAX) | |

| Edinburgh Investment Trust (EDIN) | Impact Healthcare (IHR) | |

| Twenty Four Monthly Income (SMIF) | ||

| Honeycomb Investment Trust (HONY) | ||

| SuRo Capital (SSSS) | ||

| Vanguard World (VWRL) | ||

| Assetco (ASTO) | ||

| Henderson High Income (HHI) | ||

| JP Morgan Global Growth & Income (JGGI) | ||

| Digital 9 (DGI9) | ||

| Foresight Solar (FSFL) |

The New Kids

As has become customary on this blog, I like to say a few words about new portfolio entrants of which there are quite a few this quarter. My investment company holdings are mainly focused on income at a reasonable price (EPIC, IHR, SMIF, HONY, HHI, DGI9, FSFL) with a handful more growth focused while also paying a dividend (APAX, SSSS, VWRL, JGGI). And that leaves three new direct equity holdings:

Record (REC) – a specialist (currency hedging) asset manager. It has always been a high quality company paying a reliable dividend but previously lacked growth. That appears to be changing under the guidance of a relatively new CEO, so I have jumped aboard for the ride.

Arqit Quantum (ARQQ) – a new cybersecurity entrant (a UK company listing on Nasdaq via a SPAC) focused on protecting the world against the cyber threat facilitated by quantum computing. Their QuantumCloud platform has a potential market of every device that is connected to the internet. Arqit claim to have created a simple yet elegant solution to the threat and are now moving to scale up via a host of Tier 1 partners/customers and the US/UK government. I might be delusional but I have a strong hunch about this one and have invested around 2.5% of my portfolio by value on the basis that if I am right, it will make me many multiples of my original investment. My intention is to review that decision in around five years. Between now and then, ARQQ has much to prove and hopefully, it will deliver.

Assetco (ASTO) – another asset manager, making it the fourth in my portfolio. It is a buy and build company (from a cash shell) which carries higher risk. However, the management team are from Aberdeen Asset Management from a time when they still used vowels and I like the look of their strategy, so again, I have hopped aboard for the ride.

Dividend Update

As at the end of Q3, dividend income has been almost exactly 75% of my annual forecast. Having halved my position in AAZ during the quarter (and before payment of the interim dividend), I might fall slightly short of that forecast for the full year. This should be offset by an increase in the forecast for 2022.

Portfolio Characteristics

Given the revised structure of the portfolio, I have updated the portfolio characteristics that I measure. I have dropped the “strategy” component (i.e. Value, Income, Quality/Growth). In essence, the Investment Company holdings are mainly income with some growth and the Direct Equity holdings are mainly growth with some income which is reflected in the following summary:

| Number | Weight | Average Yield | Average Volatility | Average Discount/Premium | Average Q/V/M | |

| Direct Equities | 16 | 63.73% | 2.80% | 3.25 | N/A | 86/39/51 |

| Funds (ITs/ETFs) | 16 | 36.09% | 5.96% | 2.06 | -2.21% | N/A |

Combined Yield (weighted) = 4.12%

Combined Volatility (weighted) = 2.89 (Adventurous)

Going forward, this is how I shall review the portfolio characteristics each quarter, as captured on this page.

News flow and Outlook

I really must get back to writing Share Watch articles to reflect on news flow as the quarter unfolds. By the time it gets to this quarterly review, there is simply too much to comment on. For the most part, companies delivering trading updates and/or results were in line or ahead while outlooks have remained broadly positive, perhaps dampening expectations in some instances. As per the macro comments below, I am expecting business conditions to become tougher during the final quarter and into the start of next year.

This said, the most significant news came a couple of days before the end of the quarter, although you wouldn’t guess that from the stifled share price reaction. Anglo Asian Mining (AAZ) have finally concluded contract negotiations with the government and as a result, have been awarded significant new contract areas, subject to ratification in parliament. This provides a clear path to mid-tier level production for this gold/copper miner. I look forward to further updates from the company regarding the plan and timeframe for bringing these assets into production.

I anticipate that news flow from the trading companies will be quiet in Q4 while management teams get on with closing out the year, although I am looking forward to results/updates from Bioventix (BVXP) and several of the financials/asset managers. Additionally, I am keen to see NAV updates for several of the property companies where hopefully, there will be some upgrades.

Macro Observations

Where to start? I guess the headline story is that inflation is raging and no longer looks as though it will be transitory. While commodity prices have moderated somewhat this quarter, energy prices are flying, as are shipping costs. When combined with supply bottlenecks and shortages (including food and labour), we might be heading toward a winter of discontent. The next phase is likely to be rising wages to attract and retain labour which will only serve to fuel inflation further and limit the chances of it being transitory.

But then what? In my view, this is not good inflation driven by productive growth. It is the type of inflation that kills growth via a vicious circle of rising costs and higher prices for non-discretionary goods and services. This leaves less of the pie for discretionary spend, absent rising wages. If central banks (led by the Fed) intervene by raising rates (and the bond market seems to be suggesting that they will), what will be the impact on debt (retail, corporate and government)? And how will that impact growth? Stagflation anyone?

Meanwhile, China continues to tread its own path and who knows where that will end or how the US will respond? I suspect we will be hearing more about their digital currency now that they have banned cryptocurrencies.

In many respects, I am pleased that markets have begun to correct during September. It means they are functioning as they should and pricing for increased risks. In particular, long dated securities (e.g. growth shares) become less attractive IF rates were to rise. And that’s what I have seen happening over the past couple of weeks – a contraction of PE ratios across many highly rated shares. I also sense tougher business conditions across the board, although so far, my own portfolio holdings have traded well and not had to issue any profit warnings. This said, a few of them have dampened expectations which is also probably a good thing. If we do head towards a stagflation scenario, I don’t expect the companies I own to be immune but I do expect them to be resilient, as that is part of my selection criteria.

I shall leave you with a final macro thought. What if the Fed doesn’t raise rates? I imagine owning gold or gold producers would be part of the answer, perhaps!

Cheers

Simon

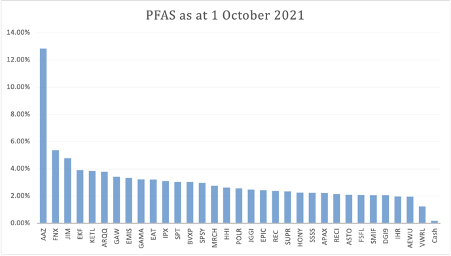

Disclosure – At the time of writing, the companies I own shares in are as per the graphic below. If you are reading this in the future, my latest published list of holdings/weightings can be viewed here.