It is six years since I embarked on my mission to construct a portfolio that would serve my family’s investment needs in all market conditions – an all-weather portfolio. Hence naming the portfolio PFAS (Portfolio for All Seasons). The portfolio remains a work-in-progress (in truth, it probably always will) and I have devoted the final section of this article to laying out my thoughts on the current construct of the portfolio.

Before then, I shall be reviewing the key portfolio metrics for 2021 and making some macro observations vis-à-vis the main scenarios and trends I will be looking out for in the year ahead.

A Review of 2021

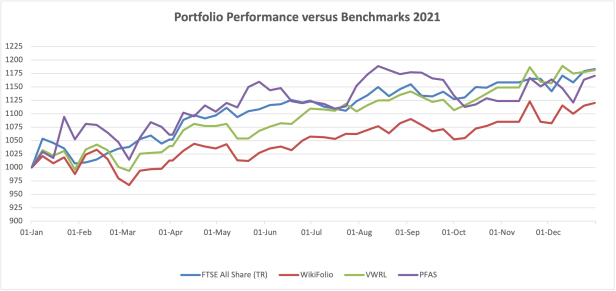

A blow-by-blow account of how my year unfolded can be viewed via my Twitter thread of weekly updates While not a vintage year, the total return for PFAS in 2021 was 17% which I regard as satisfactory. It is good to exceed my minimum absolute return target of 10%, although slightly disappointing to dip below my main benchmarks, FTSE All Share TR (+18%) and Vanguard World ETF (VWRL) (also +18%), in the final few weeks of the year. Perhaps most importantly, both capital and dividend growth were ahead of inflation which remains a key area of focus for me going into 2022. Unsurprisingly, the portfolio’s CAGR since inception (6 years) has now fallen to 28.25% and remains far ahead of my long-term expectations.

Dividends exceeded my start of year forecast by 5% and next year’s forecast is raised by 8% year-on-year. This is particularly pleasing as there have been no dividend cuts this year and many portfolio companies have been able to pay increased and/or special dividends.

There have been no major profit warnings (some dampening of expectations) and no takeovers within the past year. The last time there were any takeovers in my portfolio was between March and May 2019 when I had three in quick succession.

Main Winners and Losers

| Top 3 Contributors | Top 3 Detractors |

| Arqit Quantum (ARQQ) +139% | Bioventix (BVXP) –21% |

| Impax Asset Management (IPX) +110% | Anglo Asian Mining (AAZ) -13% |

| Jarvis Securities (JIM) +31% | Games Workshop (GAW) -12% |

This table pretty much sums up the whole of my investing year. A couple of very decent winners and a good supporting cast dragged back by poor performance from a few larger holdings, especially when one of those holdings, Anglo Asian Mining (AAZ), started and ended the year as my largest position. As highlighted in my Q3 review I halved this position in the second half of the year which is a decision I remain comfortable with, even if AAZ were to double in the year ahead (now, that would be nice!).

Both Impax and Arqit are worthy of special mention. Impax (IPX) has been in the top contributor column throughout the year, performance that is backed up by record AuM inflows and strong investment performance. While expensive both then and now, they are benefitting from structural tailwinds and, despite top slicing around 35% of my holding during the year, they remain a core, top ten holding. Arqit (ARQQ) was but a twinkle in the market’s eye at the beginning of 2021 and has delivered a remarkable 139% return since its IPO in early September (I invested pre-IPO via a SPAC in August). They have been even higher than that and I top sliced a third of my holding in the mid $30s, returning my invested capital in its entirety. Even though this is a pre-profit company and therefore, a highly speculative investment proposition, I am happy to stay on board for the ride (at ~4% portfolio weighting). You never know, it could be THE one! Perhaps?

Moment of Truth

Thanks to ‘cockerhoop’ on Twitter, we now have a new name for this section of the review – the Meddling Quotient. That is, how does actual performance compare to the performance if one had not tinkered at all?

I am pleased to record that this year my meddling has added 9.12 percentage points to my performance (i.e. 17.06% actual performance versus 7.94% if I had left my portfolio unchanged from the start of the year). Perhaps I won’t berate myself too much for overtrading this year!

Portfolio Changes

Of the 24 holdings at the start of the year, only 11 remain. For the record, I exited III, AVST, BRWM, FDM, HFEL, HINT, IGG, QTX, RCH, SMS, SPSY and KETL. I have added a net 21 holdings to the portfolio and as covered in my Q3 review, much of this related to adding more investment trusts to my portfolio to diversify dividend income. The new holdings this year are AEWU, APAX, BMY, DGI9, EPIC, EAT, FNX, FSFL, HONY, IHR, MONY, PAY, POLY, PEY, RECI, SOM, SUP, XPP, ARQQ, SSSS and VWRL. And with tongue firmly in cheek, I shall conveniently forget about those holdings that both entered and exited the portfolio this year by simply referring you to my Meddling Quotient of +9.12% 🙂

Portfolio Metrics

I finish the year with 19 direct equity holdings and 14 funds (13 ITs and 1 ETF). The direct equity holdings carry just over two thirds portfolio weight while the funds are responsible for around two thirds of overall portfolio income. This breakdown can be seen on the Performance and Analysis page

I am pleased to be maintaining a natural yield above 4% while also growing the capital at a decent clip. This said, I would like to reduce the portfolio’s volatility a little in the year ahead. The fund segment of the portfolio has moved from a small discount (on average) to a slight premium.

Macro Observations

As ever, I do not pretend to have any sort of crystal ball or edge when it comes to the macro environment but nonetheless, it provides the context in which we invest and live our lives. While my individual stock picks are all selected on a bottom-up analysis, I do pay some attention to top-down macro factors when it comes to overall asset allocation.

2022 is the year in which we will discover if inflation is transitory or whether it becomes more embedded. While year-on-year comparatives will begin to slow from the second quarter and supply chain issues and energy/commodity prices might begin to ease, I believe the higher probability is that now the inflation genie has been let out of the bottle it will take significant central bank intervention to get it back under control. Will the Fed conclude their bond buying by the end of March? Will we see a taper tantrum? Will the Fed, ECB, BoE raise rates? At what pace?

I don’t envy the central bankers. Raise rates too slowly and inflation gathers pace, raise too much too soon and the global economy will be pushed into recession, creating a stagflation environment.

What is The Great Reset? I have heard people mention this term and thought it was just another conspiracy theory but then I noticed that it was the title of this year’s Davos conference (postponed until summer 2022). Perhaps it is just a marketing slogan?

2022 will also be the year when we learn more about Central Bank Digital Currencies (CBDCs), some of which have already soft launched (e.g. China). How will these digital currencies work? Will they replace crypto or operate alongside? Will they lead to currency wars? Will they be the prelude to split East/West economies, signalling the end of globalisation as we know it?

Perhaps the preceding two paragraphs should be joined into one? Or perhaps there is nothing significant about CBDCs other than improving payment processing and making our lives easier? It will be interesting, if also a little scary, to discover more about CBDCs as the year unfolds.

And of course, there are geopolitical tensions wherever one looks, such as Russia/Ukraine/The West and China/Taiwan/The West.

The US looks overvalued with surplus liquidity in the system (e.g. SPACs, NFTs, IPOs and meme stocks). Perhaps we will have another taper tantrum in March/April? Or, if we actually see rising interest rates, one imagines the shift from growth to value will continue. On the plus side, the Omicron variant seems to be taking us toward herd immunity while hopefully avoiding another lockdown. On balance, I believe the UK market looks undervalued or at least, there appear to be decent pockets of value in the UK market.

We shall see!

Portfolio Construct

Observing the macro environment is one thing but devising a strategy or constructing a portfolio to survive and thrive is another matter altogether. I view my current portfolio as being 3 segments (portfolio weightings in brackets).

18 Direct Equity Holdings (64%)

12 Investment Trusts (28%)

3 Wildcards (8%)

The Direct Equity Holdings

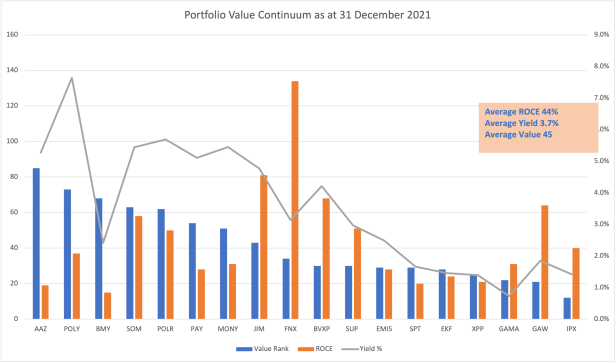

All 18 holdings in this segment fall under the banner of Quality Compounder. That is, I like to invest in high quality companies with strong cashflows that reinvest profits for further growth, returning any surplus to shareholders via a dividend. My investment strategy is depicted by the following graphic which shows each holding on a valuation continuum (using the Stockopedia Value Rank) alongside the latest Return on Capital (ROCE) figure and overlaid with the dividend yield. This segment of the portfolio is exclusively UK listed small/midcaps (i.e. Larger than £100m market capitalisation and less than £10bn).

At the value end of the continuum, there are stocks that are cheap for a reason such as cyclicality (e.g. AAZ, POLY, SOM), recoveries-in-progress (e.g. PAY, MONY) or market risk (e.g. POLR). In that context, Bloomsbury Publishing (BMY) looks particularly good value and not particularly cyclical given the digital transformation that is underway in their academia division (the current broker forecasts also look very conservative to me). At the other end of the spectrum, there are companies such as Games Workshop (GAW), Gamma Communications (GAMA) and Impax Asset Management (IPX) that remain relatively expensive and vulnerable to the downward re-rating of long-dated securities (e.g. growth stocks). This said, they all have the ability to continue growing and exceeding current market forecasts but nonetheless, they carry meaningful valuation risk.

The Investment Trusts

I currently have 12 UK listed Investment Trusts. These are held mainly for income but with some elements of growth. They also help to reduce portfolio volatility. Current holdings and key metrics are as per the graphic below (along with a plug for the increasingly useful AIC website). It is worth noting that I have recently reduced exposure to equity income funds, retaining only Merchants Trust (MRCH) in that category. I plan to add a couple more large cap equity funds during 2022, once the direction of travel becomes clearer.

Some of these holdings pay a dividend from income. This would include Merchants Trust and all the REITs (Real Estate Investment Trusts). However, some of these holdings pay income out of capital. This would include the private equity companies which both pay 5% NAV as a dividend and European Assets Trust paying 6%. I quite like this approach (as opposed to realising capital gains myself) and see no problem with it while NAV is growing, although I might change my mind in a bear market.

The Wildcards

Vanguard World ETF (VWRL) – This is not so much a wildcard but rather, it is my main benchmark and the product where I would place the majority of my capital if I ever give up active investing or indeed, how my family are guided to invest the funds they will inherit.

Arqit Quantum (ARQQ) – A company I have mentioned earlier in this piece but a real wildcard from an investment perspective. I have been waiting a long time to find the next UK tech giant (the last one in my view was ARM Holdings which I sold far too soon) and I think ARQQ might in time prove to be in that category (perhaps understandably, they chose to list on Nasdaq). They offer a cybersecurity solution that potentially can be used to protect every internet connected device while being future proofed to handle threats from quantum computing. As stated earlier, I have already recovered my initial investment and at a stock specific level, I am now on a ‘free ride’. But boy oh boy, the share price is extremely volatile.

SuRo Capital (SSSS) – This is a late-stage venture capital company with decent deal flow. Similar to UK REITs, this company is obliged to return 90% of investment returns as dividends. Around 60% of their NAV was returned in 2021. Let’s hope for more of the same in 2022. So far, I have received around 13% of my investment back via dividends (c10% cash and c3% shares) and seen a further dividend declaration in December. I’m sure this holding will suffer if/when the taps are turned off the IPO market, so it may only be a transient holding.

A portfolio for all seasons? As ever, history will be my judge.

An Unfinished Jigsaw

I am not yet totally comfortable with the portfolio, although I hope to avoid any wholesale changes in the year ahead. I have a very small watchlist of direct equities and I also have my eye on a couple of additional investment trusts. There are a few holdings that I imagine will be transient but most I intend to hold for the long-term. This said, if the move away from long-dated securities gathers pace, I might feel compelled to review those holdings and perhaps move to protect capital.

For the past few years, I have tweeted a weekly portfolio update, covering weekly movements, YTD tracking, trades and RNSs among portfolio components. While it does provide some benefits such as a weekly diary, I have decided to end this practice and zoom out a little. Going forward, I shall be reviewing my portfolio quarterly on this site and perhaps adding occasional Share Watch articles when news flow is particularly interesting or significant. As for Twitter, gawd knows what I’m going to contribute – perhaps I need to get better at memes!

I wish all readers a happy, healthy and prosperous 2022.

Simon

@BrilliantLeader

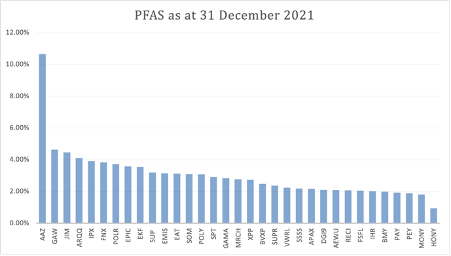

Disclosure – At the time of writing, I own shares in all of the holdings in the graphic below or, if you are reading this in the future, my latest holdings declaration can be seen here

Hi Simon

Just a quick note to say how much I value your posts. I have been taking a much keener interest in equities over the last few years as I approach the point where I have to live off my savings….! I find the prospect quite scary, but not so scary to pass the opportunity to the so called ‘wealth managers’.

I rarely post on stocko or twitter as I’m still learning, but am looking forward to spending more time researching & comminicating as my investment journey progrsses.

With very best wishes

Simon

LikeLike

Thanks for dropping by Simon and I’m glad my musings are of value.

LikeLike