Everyone and their dog seems to have been speaking about coffee can stocks this quarter, especially if one regularly follows the Small Cap Value Report (SCVR) on Stockopedia – indeed, there is a thread specifically set up for people to discuss their coffee can stocks. For the uninitiated, a coffee can stock is one that you intend to buy and forget, potentially holding forever as opposed to coffee cup stocks (my label) that are more transient in one’s portfolio. The analogy is that people often kept/keep their rainy day money hidden away in a coffee can and often forgotten about. I remember when my grandmother passed away we found a couple of thousand pounds in cash stashed away in, in her case, a biscuit tin.

My own view is that, theoretically at least, every stock I own is a coffee can stock unless/until the investment thesis fails. But in reality, some holdings are higher conviction and more embedded in my portfolio than others. So, for a bit of variety in this mid-year portfolio review, I thought I would run my entire portfolio (direct equity holdings only) through a coffee filter (see what I did there!?), highlighting the main basis of my investment thesis and in true tabloid fashion, a coffee can rating out of 10.

But first, I shall run through the quarterly portfolio metrics at this half-way point in the year.

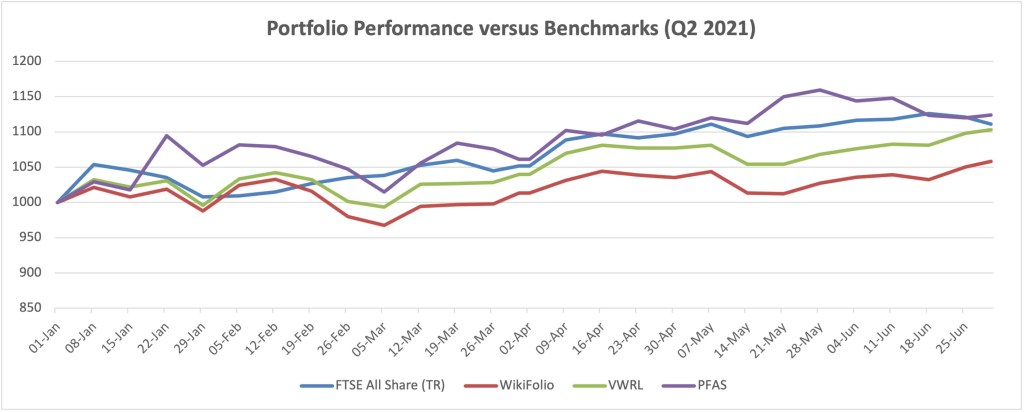

Performance versus Benchmarks

A satisfactory performance this quarter, supported by in-line or ahead statements from virtually all holdings and without many fireworks in either direction. My portfolio (PFAS) was up 5.92% for the quarter (+12.41% YTD) which was slightly behind the Vanguard World ETF (VWRL) at 6.06% for the quarter (+10.3% YTD) but ahead of the FTSE All Share TR index at 5.61% for the quarter (+11.09% YTD) and my Wikifolio ETF which is lagging with a +4.47% quarterly performance (+5.84% YTD).

At the beginning of every year, I would gladly take a 25% return and so, in absolute terms I have to be content with being on track for that at the mid-year point. On a YTD basis I am also running ahead of all three benchmarks – again something to be satisfied with. Nonetheless, in golfing parlance I feel I have left a few shots on the course. This is also reflected in a declining momentum score which is something I am mindful of – perhaps some of my value/contrarian plays will provide a spark or two in the second half to reverse that trend.

For the most part though, I am concerned with analysing the business performance of my holdings rather than the share price performance. And on that front I am very pleased with the progress being made by all holdings and mainly, broker forecasts still seem to be on the conservative side. That said, trading updates will be coming thick and fast during July, so the verification process continues.

Contributors and Detractors

| Top 5 Contributors (Q2) | Top 5 Detractors (Q2) |

| Impax (IPX) +46% | Fonix Mobile (FNX) -13% |

| Gamma Communications (GAMA) +19% | Spectra Systems (SPSY) -6% |

| Polar Capital (POLR) +19% | EKF Diagnostics (EKF) -5% |

| Strix Group (KETL) +17% | Bioventix (BVXP) -3% |

| Games Workshop (GAW) +16% | Henderson Far East Income -0.6% |

Impax (IPX) continues to knock it out of the park (+57% YTD) enjoying some strong, structural tailwinds. Also making a second appearance in the top quarterly contributors list is Strix (KETL) for a highly respectable 41% YTD. Against that, Bioventix (BVXP) and Henderson Far East Income (HFEL) both appear in the top detractors list for the second quarter running, albeit for more modest YTD losses of 8.5% and 1.5%, respectively. It is also pleasing to note that both Gamma Communications (GAMA) and Games Workshop (GAW) have reversed last quarter’s declines and are into positive territory for the YTD. I shall be looking out for the next Fonix Mobile (FNX) trading update with particular interest as I have “taken advantage” of recent share price weakness to top up my holding – their update will be for the full year ending 30 June and they were ahead at the halfway stage, so let’s see.

Portfolio Changes

| Exit | New |

| Vanguard Emerging Markets ETF (VFEM) | Polymetals International (POLY) |

| Rio Tinto (RIO) | European Assets Trust (EAT) |

| Sylvania Platinum (SLP) | AEW UK REIT (AEWU) |

| Personal Group (PGH) | |

| Real Estate Credit Investments (RECI) |

Additionally, there were various top slices and top ups of existing holdings, as per my process (and as captured on my weekly Twitter updates). The sales are mostly as a result of a strengthening dollar (VFEM) and weakening commodity prices (RIO, SLP) – in truth, too many commodities for me to be paying attention to. POLY was added as a large cap gold/copper holding which unlike Anglo Asian Mining (AAZ), tends to move in synch with the gold price. PGH is a value/recovery play and a former holding while EAT, AEUK and RECI have been added to diversify income.

Portfolio Characteristics

Q1 figures are in brackets.

Natural portfolio yield 4.08% (4.07%), Quality 85 (87), Value 47 (43), Momentum 55 (64) and a weighted volatility of 2.89 (2.98). If it were a single entity PFAS would have moved from being an adventurous high flyer (to use the Stockopedia lingo) to adventurous neutral due to the declining momentum rank. The big question in the second half will be whether it returns to being a high flyer or heaven forbid, sinks to fallen star status. Obviously, I shall be hoping for the former.

Newsflow and Outlook

In addition to the plethora of trading updates and results that will come my way in Q3, I also expect a fund raise from Smart Metering Systems (SMS) to invest in the next phase of CaRe assets (my assumption), a special dividend from Jarvis Securities (JIM) following the cancellation of the share premium account (perhaps) and for AAZ to issue a maiden JORC for the Zafar mine (and perhaps news of expanded contract areas). It should be an interesting period, perhaps even exciting.

Macro Footnote

It is no longer a case of whether we get inflation or not but rather, whether it will be transitory, as the Fed suggests, or something that needs to be dealt with via tighter monetary policy. Certainly, the headline numbers are coming from a low base and while commodities are off all-time highs, they remain at the upper end of the recent range. Multiple companies are beginning to report rising input costs and supply chain bottlenecks. It is too hard and too early to call in my view but there was an excellent piece by one of my favourite macro commentators, Edmund Shing of BNP Paribas Wealth Management – readers might find it useful to see Edmund’s take on what type of companies might thrive in an inflationary environment

Basel III appears to have been a damp squib given the LBMA’s exemption from participating (granted by the Bank of England) until 1st January 2022 at the earliest which probably enables the can to be kicked down the road and the trading in unallocated gold to continue. Nonetheless, I shall maintain a watching brief on developments. Similarly, I shall maintain a watching brief on the development of Central Bank Digital Currencies (CBDCs) which look to be coming our way in 2022. This said, I have no idea what impact they might have other than increasing the regulation of cryptocurrencies. Watch this space!

Coffee Can Analysis

Anglo Asian Mining (AAZ) – A low cost, debt free, cash generative gold/copper miner that returns surplus cash to shareholders via dividends (circa 5%). But, it also has significant exploration upside which means they are likely to be mining and paying a dividend long after I am propping up daisies. This said, there are a couple of factors that would prompt me to exit, including structural decline in commodity pricing and the departure of the CEO (depending on the succession plan). Coffee Can Rating 8/10

Bioventix (BVXP) – A company that generates royalty type revenues from the licensing and sale of bovine monoclonal antibodies. These are used in a range of diagnostic tests. Growth has stalled recently but should get back on track as the royalties on Siemen’s Troponin test ramp up. Current R&D is focused on revenues 5-10 years in the future which makes this very close to a perfect rating. However, my holding is dependent on the Founder/CEO remaining in role as I cannot see an obvious successor. Coffee Can Rating 9/10

EKF Diagnostics (EKF) – A multi-faceted medical diagnostics company with some significant short and mid term growth drivers. It is one to hold so long as execution and growth remain on track. Coffee Can Rating 6/10

Emis (EMIS) – A software company with a high dependency on the NHS. A new version of their platform and the expansion into the private healthcare market presents the growth opportunity. Again, it is one I intend to hold so long as execution and growth remain on track. Coffee Can Rating 6/10

Fonix Mobile (FNX) – A mobile payments provider. Their platform provides an interface between consumers and businesses that enables payments to be made by text (think Children in Need, for example). The growth opportunity comes from winning new customers, in new verticals and also geographical expansion (e.g. Europe). There is probably a lifespan for this technology, so my holding period is likely to be limited by that and the company’s ability to evolve their offering. Coffee Can Rating 7/10

Games Workshop (GAW) – A large and rapidly growing hobby business. The business has come a long way under the stewardship of current CEO Kevin Rountree and it will be interesting to see how far he will be able to take it. I will probably be a seller when Kevin stands down, although I am open to being convinced on the succession because the hobby is set for a bright future. Coffee Can Rating 8/10

Gama Communications (GAMA) – A unified communications provider with a combination of organic and acquisitive growth. One to hold so long as execution and growth remain on track. Coffee Can Rating 7/10

Impax Asset Management (IPX) – A specialist asset manager in the ESG space that is growing rapidly thanks to the scalability of its offering and the structural tailwinds of money looking for ESG friendly funds. I’m not sure that trend is going away anytime soon, so it is hopefully one I will continue to hold for a while yet. Again, I would also be influenced by the tenure of the Founder CEO. Coffee Can Rating 8/10

Jarvis Securities (JIM) – A low cost online stockbroker and provider of custodian services. It is highly profitable and capital light and returns surplus cash to shareholders via a quarterly dividend. Ultimately, I expect my exit to be influenced by the tenure of the Founder CEO. Coffee Can Rating 8/10

Personal Group (PGH) – A niche insurance provider in the employee benefits space. It is dependent on its salesforce’s ability to sell, although the pandemic has led to investment in its platforms and strategic partnerships (e.g. Sage) which should diversify income streams over the medium term. This said, I think there is plenty of execution risk with this business and a future profit warning might trigger my eventual exit – perhaps. Coffee Can Rating 6/10

Polar Capital Holdings (POLR) – An active fund manager that grows organically and by acquisition. Its profits are highly dependent on funds under management and performance fees and will therefore suffer in a bear market. I would also argue that active fund managers continue to be under pressure to reduce fees under increasing competition from ETFs. Coffee Can Rating 4/10

Polymetal International (POLY) – A gold/copper producer with multiple mines in Russia and one in Kazakhstan. It is a relatively low cost producer but with a share price that is dependent on the commodity prices. This is probably a relatively short-term hold for me. Coffee Can Rating 3/10

Smart Metering Systems (SMS) – A provider of smart meters which generate a royalty type revenue with growth coming from their expanding portfolio of CaRe (Carbon Reducing) assets. My holding period will be defined by the evolution of the business over the longer term. Coffee Can Rating 8/10

Spectra Systems (SPSY) – A multi-faceted company with the core business providing security materials for the production of banknotes. Their clients are central banks and these contracts are long-term in nature, providing good and stable forward visibility of earnings. The growth opportunity comes from a number of other technologies the company is working on such as Trubrand to fight against, among other things, counterfeit tobacco in China. Another company with a key man at the helm, the departure of whom would likely be my own cue to exit. Coffee Can Rating 6/10

Spirent Communications (SPT) – A provider of testing products and services for the telecoms industry. The key growth driver is the 5G rollout which should create significant opportunities for the company. My own holding period will be driven by the growth and execution. Coffee Can Rating 6/10

Strix (KETL) – A company with extensive IP in kettle controls and more recently (via acquisition) water products. Another holding that will be driven by the growth and execution. Coffee Can Rating 6/10

This has been an interesting exercise that has helped me think about what might cause me to sell each of my holdings. The two main themes that emerge are 1) business performance/growth prospects and 2) a key person risk (e.g. Founder/CEO). It has also helped me identify a couple of holdings where I have quite low conviction which has given me some pause for thought.

And Finally…

The most important thing that has happened during the quarter has been the birth of my first grandchild, Harvey who has taken up much more of my time than investing. I also opened a Junior ISA for him and put it all into the Vanguard World ETF (VWRL), so I will forgive him for beating me this quarter (beginners’ luck!) but I shall be gunning for him in Q3.

I wish all readers a healthy and successful third quarter and perhaps a few days off to find some elusive British sunshine.

Cheers

Simon (@BrilliantLeader on Twitter and crazycoops on Stockopedia)

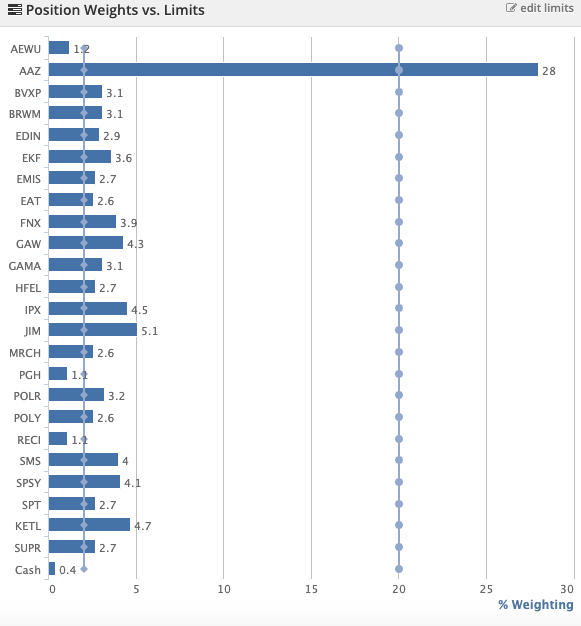

Disclosure – At the time of writing, I own most of the stocks mentioned in this article (as per the graphic below). Or if you are reading this in the future, my most recent holdings declaration can be viewed here

Holdings as at 30 June 2021