Welcome to my first quarterly review of 2021 where it has been a positive, albeit volatile, start to the year for my portfolio (PFAS). For context, I will be referencing several items from my year-end review which can be opened here in a new window/tab.

Performance versus Benchmarks

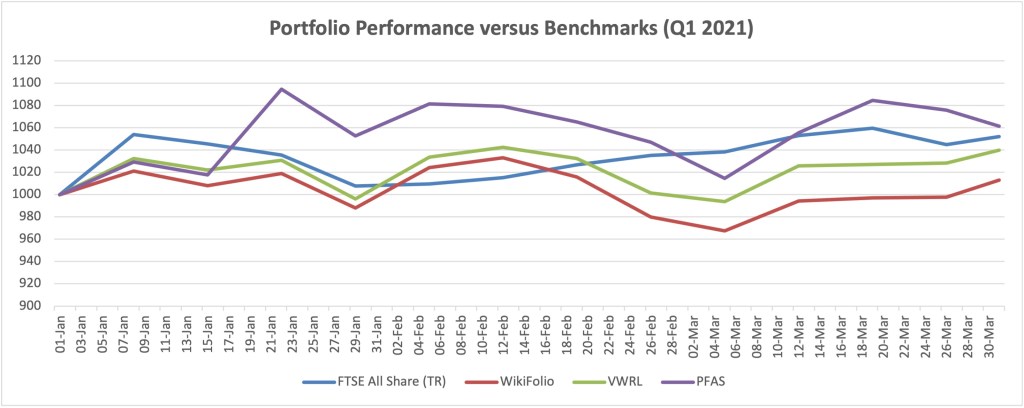

PFAS was up 6.12% for the quarter which compared favourably to the three benchmarks I use; FTSE All Share TR +5.19%, Vanguard World (VWRL) +3.99% and my Wikifolio ETF portfolio +1.31%. This said, it was up 10% in January before falling back through February to 1% and recovering during March, as per the chart below:

Contributors and Detractors

| Top 5 Contributors (Q1) | Top 5 Detractors (Q1) |

| Fonix Mobile (FNX) +24% | Games Workshop (GAW) -10% |

| Strix (KETL) +22% | Spirent Communications (SPT) -7% |

| Smart Metering Systems (SMS) +16% | Bioventix (BVXP) -6% |

| Jarvis Securities (JIM) +15% | Gama Communications (GAMA) -0.3% |

| Impax Asset Management (IPX) +11% | Henderson Far East Income (HFEL) -0.15% |

Interestingly, 3 of the top 4 detractors were all highlighted in my year end review as carrying valuation risk. This said, I am happy with the results/outlook from these holdings and three of them (GAW, SPT, GAMA) I have topped up during the quarter.

In terms of the top contributors, they have all delivered excellent results/outlook and have re-rated accordingly. I’m not sure this outcome fully supports the narrative that there is a significant rotation from value to growth in progress, although perhaps IPX can be viewed as an anomaly (they are knocking it out of the park with both net inflows and fund performance). The other four (FNX, KETL, SMS, JIM) all offer growth at a reasonable price, underpinned by decent and growing dividends.

Portfolio Changes

| Exit | In/Out Trades | New |

| III | UPGS | FNX |

| QTX | CEY | SLP |

| RCH | BERI | VFEM |

| HINT | FXPO | RIO |

| AVST | CLX | EDIN |

| FDM | ||

| IGG |

Too much activity (still) but in the final analysis, I fancied those that I now hold more than I fancied those that have left the portfolio, especially in relation to finding the right balance of quality and value.

Portfolio Characteristics

Year-end figures for 2020 are in brackets.

Natural portfolio yield 4.07% (4.12%). Quality 87 (84), Value 43 (38), Momentum 64 (72) and the weighted volatility of 2.98 (3.03) sees the portfolio, if it were a single entity, maintain its status as an Adventurous High Flyer.

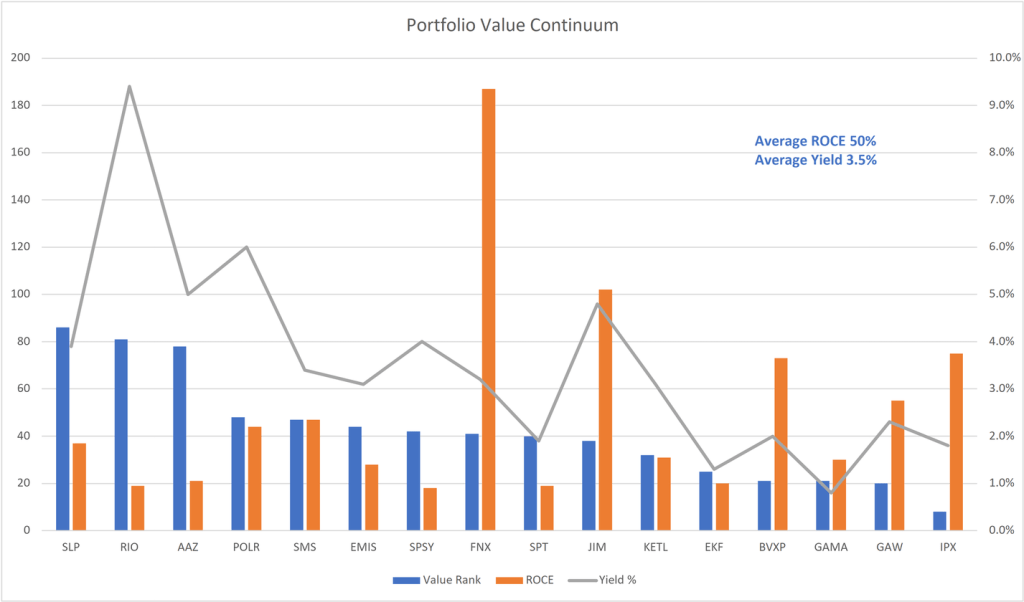

I have refreshed the portfolio value continuum with a ROCE and Dividend Yield overlay.

Average ROCE has risen to 50% (34%) thanks in large part to Fonix Mobile (FNX) entering the portfolio and average yield, excluding collective investment vehicles, is up slightly to 3.5% (3.4%). In summary, ROCE/Quality, Value and Yield all moving in the right direction while Momentum is a little weak.

Asset Allocation

I currently have 22 holdings in total – 16 direct equity holdings and 6 collective investment vehicles (5 Investment Trusts and 1 ETF). These collective investments all pay a quarterly dividend and provide exposure to parts of the market that I do not have the time/skills to address directly (they also have the useful biproduct of reducing overall portfolio volatility). These break down as follows:

Merchants Trust (MRCH) and Edinburgh Investment Trust (EDIN) – UK Large Cap Value

Blackrock World Mining (BRWM) – Global Large Cap Mining

Supermarket Income REIT (SUPR) – UK Property (or a play on UK supermarkets with higher dividend and lower risk)

Henderson Far East Income (HFEL) and Vanguard Emerging Markets ETF (VFEM) – China/Asia Large Cap Growth & Value

This motley collection is perhaps notable for its lack of exposure to either the US or Europe – areas that I aim to address in due course.

Of the 16 direct equity holdings, 4 are value plays and 12 (codenamed the dirty dozen) are quality/growth holdings that I plan to hold for the long-term (as ever, I will continue to test the investment thesis when companies report news/results).

Value Plays – Three are miners with a range of commodity exposures; SLP (Platinum, Palladium, Rhodium), AAZ (Gold, Copper), RIO (Iron Ore, Copper +++). They share a common theme of being highly profitable and cash generative at current commodity prices and a policy of returning surplus cash to shareholders via dividends. My plan is to hold them for as long as the current commodity cycle remains strong. The fourth value play is POLR where I remain mindful of the market risk that comes with asset managers. The same of course applies to IPX but their net inflows are more structural (and accordingly, the shares are more highly rated).

Quality/Growth – Putting aside the two asset managers mentioned above, the remaining holdings are BVXP, EKF, EMIS, FNX, GAW, GAMA, JIM, SMS, SPSY, SPT, KETL. In all cases, my intention is hold these for the long-term, so long as the investment thesis remains valid. Certainly, they have all delivered strong results this quarter and have plausible growth plans for 2021 and beyond.

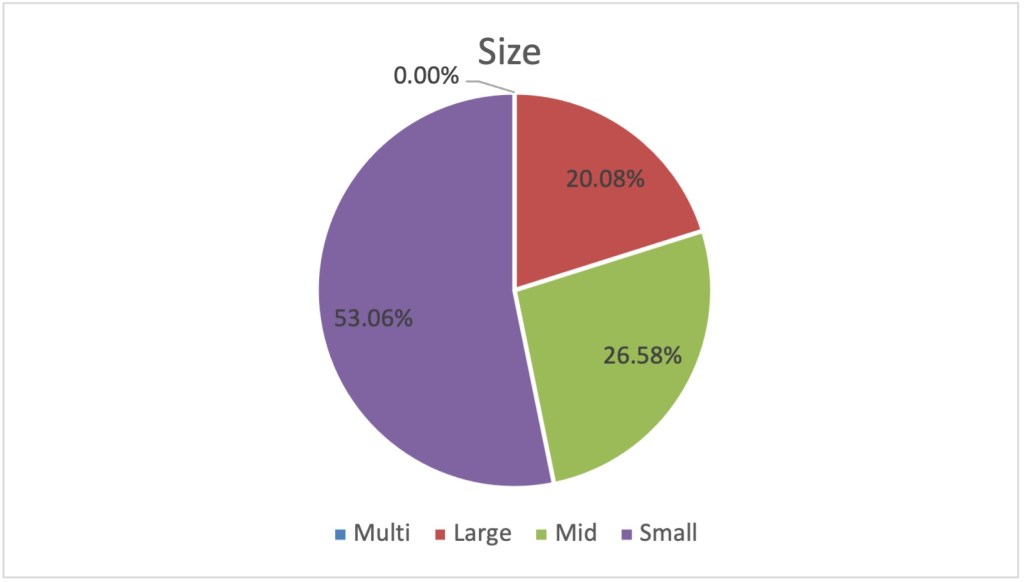

For those readers who prefer graphics, this is how overall asset allocation breaks down by size and strategy.

Macro Observations

Watching the evolving macro environment during the first quarter has been fascinating and summarised wonderfully on a weekly basis by Edmund in his Market Musings articles on Stockopedia. The market (as ever it is US led) seems to be most concerned by the prospect of inflation, stoked by both monetary and fiscal stimulus. The Fed on the other hand seem to be unconcerned by inflation, claiming that any inflation increases this year are likely to be transitory.

Certainly, many commodity prices have continued to rise throughout the quarter with the S&P global commodities index up around 15% YTD. Inevitably, this will lead to some cost-push inflation due to these higher input costs. During the second and third quarters we will see what happens when economies around the world come out of enforced hibernation. Will we get significant demand-pull inflation? Will the velocity of money increase? Will the Fed continue to let the economy run hot and for how long? How long will assets continue to inflate and what will prick the bubble? And while we are all looking at inflation, what is happening with Central Bank Digital currencies?

The other narrative in the market at the moment is the rotation from expensive growth shares to value shares, especially in relation to the reflationary trade that I discussed in my year end article. Perhaps this trend will continue or perhaps growth companies will continue to grow – a bit of both I suspect.

One final macro factor that I am keeping an eye on is Basel III which is meant to come into force (after several delays) at the end of June. I shall leave you with a recent article on the subject, should it be of interest.

In Summary

While I have some exposure to the macro factors discussed above, such as miners (SLP, AAZ, RIO, BRWM) for commodity prices/inflation protection and large cap value via investment trusts (HFEL, EDIN, MRCH), my main focus is to stick to my knitting – building positions in high quality companies that will deliver compound returns over a long period and provide me with a growing income stream in the process.

The second quarter will undoubtedly be interesting, it might even be exciting (in either a good or a bad way). I shall see you on Twitter (@BrilliantLeader) and occasionally Stockopedia (crazycoops) as it all unfolds.

Cheers

Simon

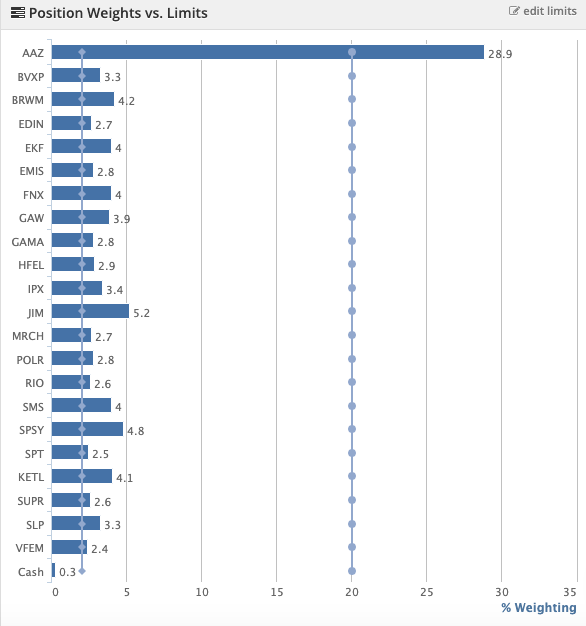

Disclosure – At the time of writing, I own most of the stocks mentioned in this article (as per the graphic below). Or if you are reading this in the future, my most recent holdings declaration can be viewed here

Holdings as at 31 March 2021