I appreciate that I am at risk of losing readers by using the year’s most overused (and hated?) word as the title for my annual review but really, it is the word that best describes 2020. Taking a global view, we have seen the sharpest, deepest market falls since 1929 and the quickest bear market of all time with a new bull market and seemingly, a new economic cycle, already underway.

The sell-off of course was the Covid-19 coronavirus pandemic causing most countries around the world to go into lockdown, versions of which most of us are still experiencing. The initial stock market recovery was triggered by massive amounts of money printing by central banks, spearheaded by the US Fed, alongside the realisation that some companies and sectors would either be benefitting from the lockdown or would not be particularly affected. More recently, the news that several vaccines* have been developed and are already being rolled out have fuelled optimism that global economies and our own lifestyles will return to normality during 2021 – the reflation trade as it is being termed.

* It is an absolutely phenomenal achievement that we have not one but three vaccines being rolled out here in the UK less than a year from the virus being discovered. Never underestimate human ingenuity!

It has certainly been a crazy year to be an investor with for example, the oil price falling to zero at one point, gold reaching new all-time highs (before falling back more recently), Nasdaq reaching new all-time highs led by the tech giants, Tesla reaching new all-time highs based on a share split (or so it seems). The range of possible outcomes for investors this year are more extreme than I have ever experienced and I am grateful to be somewhere in the middle of that particular continuum.

Apart from my quarterly updates, I have barely created any content for this site during 2020 (I will aim to put that right during 2021) as I have spent an inordinate amount of time initially researching new companies as part of my portfolio rebuild and subsequently, observing investor behaviour, learning from other investors, a deep dive into some macro topics and most importantly, learning about myself as an investor. It has been an incredible year and one that I’m sure none of us will forget in a hurry. My own chronicles of the week-by-week story as the year unfolded were captured in a Twitter thread which can be viewed here and for further context, my quarterly reviews during the year can be accessed via the quick links below which all open in a new tab.

Q1 When everything changed

Q2 Rebuilding and Rebounding

Q3 Sharpening the Saw

The Numbers

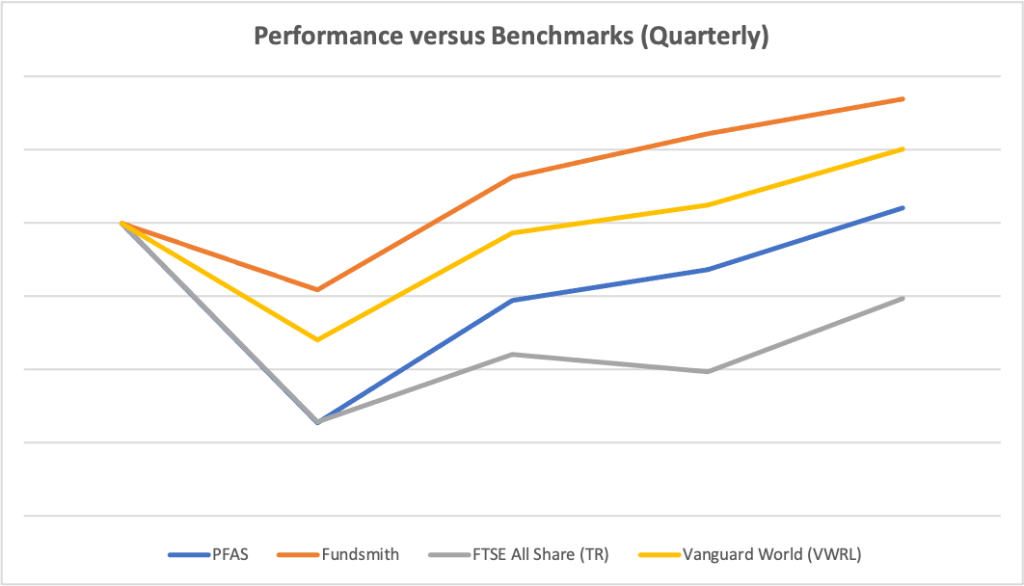

The portfolio was up during the fourth quarter by 9.06% versus 12.62% for the FTSE All Share (TR), 7.53% for Vanguard World (VWRL) and 4.14% for Fundsmith. However, it lagged both Fundsmith (+16.88%) and Vanguard World (+10.12%) with a total annual return of +2.1%, beating only the FTSE All Share (TR) which was down 10.27% for the year.

The figure that is most important to me is the 5 Year CAGR which has now fallen to 30.84%. I remain very happy with that return, despite this year’s under par performance. The full performance and analysis page can be viewed here.

Moment of Truth

Each year I like to review whether my own trading activity during the year has been profitable by comparing it to the portfolio value if I had done nothing. This year, my untouched portfolio would have been +0.7% versus a +2.1% actual return. This means that my 981 trades this year (see below) have contributed an extra 1.4% return, net of costs. It certainly doesn’t add up to a very good hourly rate this year!

Dividends

Given that it is a year when dividends were slashed by many companies, I am delighted for my dividends to have achieved 92.5% of the start of year expectations. This is thanks in large part to ~30% annual increases from AAZ, SPSY and IPX along with a nice special dividend from BVXP (quality outfits all of them!). Following the portfolio rebuild (with a focus more on total return than income), I am pleased to note that the natural yield of the portfolio is a very healthy 4.12%.

Verdict

If you had offered me a positive return for the year from 35% down in March, I would have gladly bitten your arm off. While a 63% bounce from the lows is not to be sniffed at, I am a little disappointed not to have achieved an absolute return of 10% and to be behind two out of three benchmarks. That said, the drag can be largely attributed to the lacklustre performance during Q4 of my two largest holdings AAZ and SPSY which I am confident will both come good as we move through 2021. I am also very pleased that all 24 portfolio holdings end the year in profit and with decent momentum across the board.

The Good, The Bad and The Downright Ugly

The Good

I held onto some good companies during the sell-off (e.g. BVXP, IPX). I added heavily to some core holdings close to market lows (e.g. AAZ, SPSY). I conducted a lot of rapid research to rebuild the portfolio in just a few months and to pivot again in the last quarter to add more value/recovery holdings (e.g. MRCH, RCH). All current portfolio holdings are in profit, some by more than 50% from my purchase point (e.g. JIM, III) and from a low point of minus 35%, the portfolio has recovered to plus 2.1% (a 63% bounce).

The Bad

I acted too late in responding to the initial market sell-off by underestimating the severity of the virus and governmental response. I sold some good companies (e.g. GAW, RMV). During my rebuild process, I passed on several companies that have gone on to be big winners (e.g. NCYT, CDM) and I repurchased some holdings that I should have avoided (e.g. PAY, PGH).

The Ugly

While I broadly followed my process in relation to the two pivot points we have seen in the market this year (the first being Covid/Lockdown and the second being the vaccine breakthroughs), some of my trade execution was very poor. I have made 981 trades during the year. Now, in my defence, I run several parallel portfolios, so each holding is in at least 4 portfolios (i.e. one sell/buy or top-up/top slice = minimum of four trades) but nonetheless, my execution should have been much more efficient. I reckon I should have been able to achieve a similar outcome in less than 400 trades. When I look back now at my trading journal, my activity was messy, erratic and reactive – some of this activity paid off but certainly not all of it.

Content Providers

Throughout the year, I have been an enthusiastic consumer of other people’s content. Some of this has thrown up themes/share ideas while some has served to extend my financial education and macro awareness. As well as my own participation in this craziest of market years where I have learnt much about myself as an investor, I am grateful for the learning provided by these content creators.

The End Game – a series of podcasts by Grant Williams, Bill Feckinstein and a succession of expert guests focused on the ramifications of the monetary and fiscal policy response to the pandemic crisis. They are not for the feint-hearted and will make your head spin but I highly recommend them.

PI World Educational Seminars – Tamzin at PI World created a most timely series of interviews with a range of professional investors from April onwards. Some excellent guests, providing some outstanding commentary and some very useful share ideas. And for good measure, most of them also came back during December for an end of year review. Wonderful!

Stockopedia Threads (subscription content) – My thanks to timarr for his lockdown thread, Edmund for his weekly market musings and Jack Brumby who seemed to write a research article for about half of my portfolio holdings during the year.

Twitter – As ever, I am grateful to the Fintwit community for your mutual support and collective thought on markets, themes and share ideas. I am particularly grateful to those who share their portfolios and strategy on a regular basis. Watching other investors execute their strategy is an education in itself and I thank you for sharing.

Macro Observations

I am definitely not going to make any bold predictions about the macro environment nor the impact they might have on the market. However, it does provide the context for markets and therefore, it is something I like to pay attention to. As all of my direct equity holdings are UK listed, that is the market that interests me most. But the rest of the world and in particular the US and China are also worthy of some comment.

The UK

Finally, Brexit is done and we are leaving the EU with a trade deal (on products at least). The vaccine is being rolled out. Capital flows are likely to come back into the UK market. In particular, there could be a lot of M&A activity as the UK market remains cheap on a relative basis. While I’m sure there will be some road bumps along the way (March budget, EU trade deal on services for example), I am bullish on the UK market and the ability of the UK economy to rebound.

Rest of the World

Modern Monetary Theory is taking us into unchartered waters and likely to continue down that path with a Biden presidency and Yellen at the Treasury. Nobody really knows what the impact of all this money printing will be. The early signs are that we are already seeing asset inflation, a weakening dollar, negative bond yields, negative real interest rates, a rising gold price and more recently, other commodities such as copper have been leading the reflation trade. Do these trends continue into 2021? What happens if/when the Fed switches off liquidity? How hot will the Fed let inflation run? Will the debt bubble burst? Will creative destruction be allowed to happen?

So many questions that are yet to be answered but the one that has risen to the fore of my thinking is whether the US dollar is under threat as the world’s reserve currency? In particular, 2021 will see the roll-out of China’s digital currency (DPEC). Initially, this will be domestically focused but how long before it becomes the primary currency for doing business in China or perhaps even with China. And how might the US respond? Will Facebook’s Libra digital currency ride to the rescue to provide the US with its own alternative digital currency? What does that look like and what impact will it have on the value of other currencies? Or will Central Bank Digital Currencies prove to be a red herring?

For my part, I have limited exposure to US dollar assets (I still have a number of net dollar earners in portfolio) other than via commodities where I have around one third portfolio exposure based on the current trends in both precious and base metals.

Portfolio Positioning for 2021

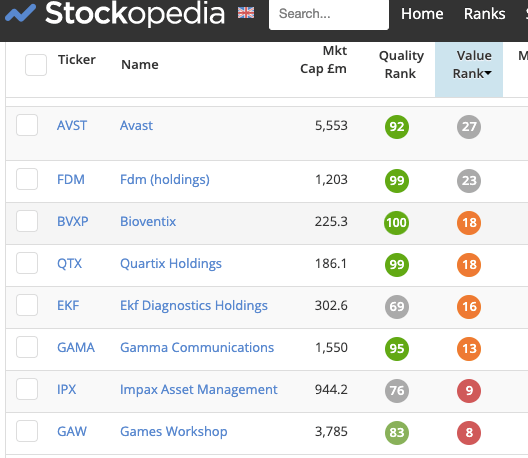

During the fourth quarter I have been making a few portfolio tweaks with a view to being well positioned for the year ahead. At a stock specific level, one of the things I am noticing is that broker forecasts appear very conservative (e.g. GAW, SPSY, EKF, QTX, RCH, SMS, GAMA, JIM) and I am hoping this leads to a string of trading updates that exceed expectations which in turn feeds through into forecast upgrades and price momentum. It is especially important for the companies with expensive valuations to deliver good trading news during the first quarter (e.g. those with a value rank below 30):

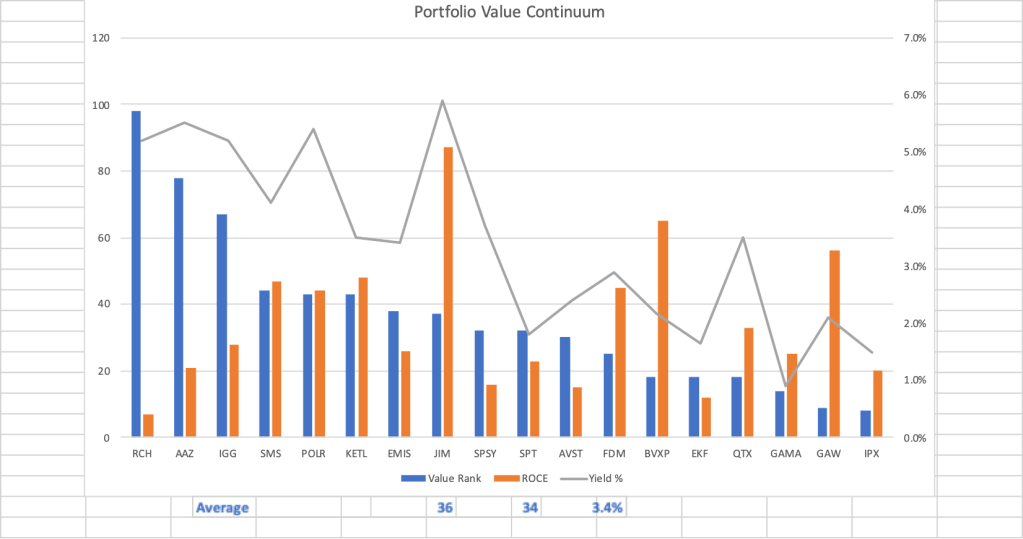

One of my favourite analyses was to view my direct equity holdings as a valuation continuum (by Stockopedia Value Rank) and overlay with the forecast dividend yield and a one-year ROCE:

An average ROCE of 34% supports my assertion that quality is the price of entry into this portfolio and provides a rule of thumb as to the type of collective return I am looking for from these holdings. It should be noted that this analysis does not include the collective investments which serve to provide exposure to other assets beyond my own UK Small/Mid Cap focus. These push up the overall portfolio yield to around 4% and also act as stabilisers on the portfolio’s volatility. However, they are unlikely as a group to return 34% per annum and therefore, also provide an intentional drag on portfolio returns.

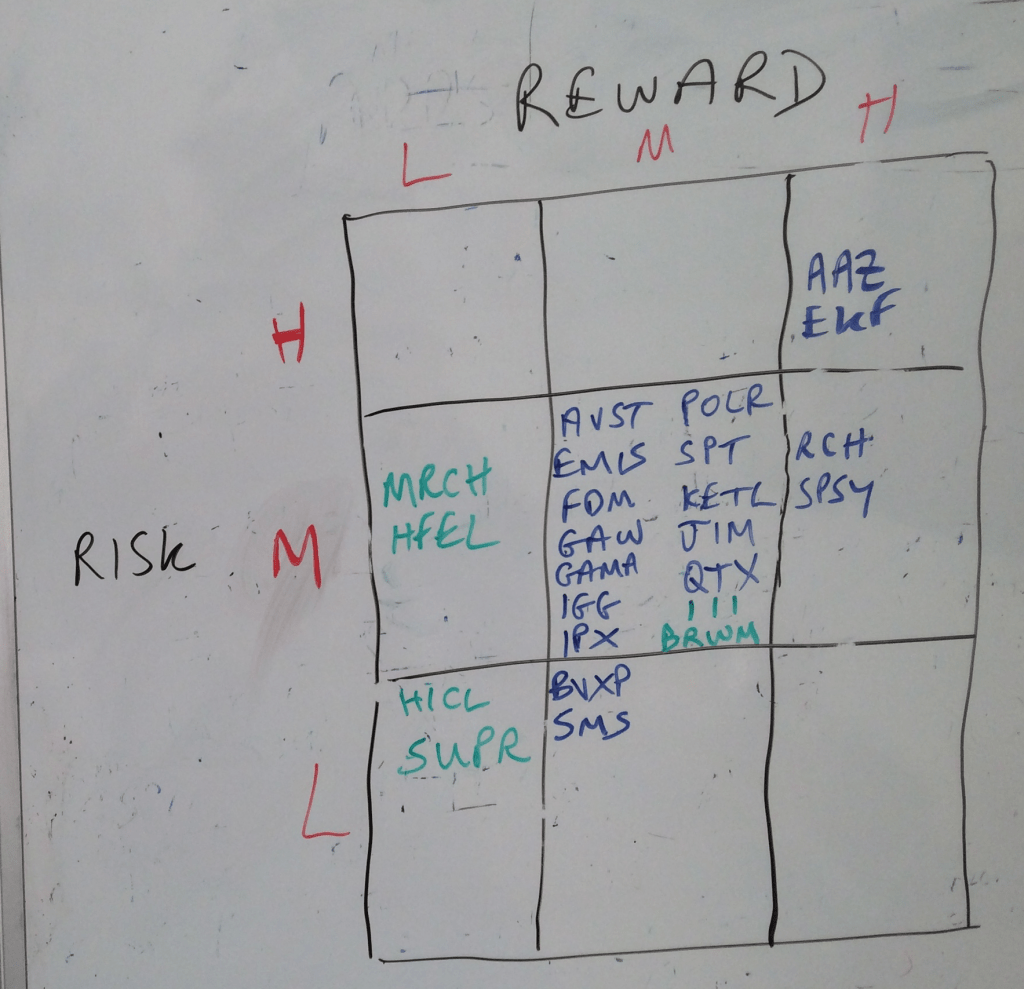

Another analysis I found valuable was a piece of whiteboarding to assess the risk-reward in the portfolio based on a 2021 view:

Of course, the flaw in this analysis is whether my assessment of risk and reward are accurate. Nonetheless, the value to me was to focus the mind on portfolio weightings and to understand how I might choose to adjust those weightings based on risk/reward factors.

The full list of current portfolio holdings and weightings can be viewed here

The portfolio had some decent momentum going into year-end – 1) break even followed by 2) all holdings in profit followed by 3) all-time portfolio high – and I hope this continues into Q1. Regardless of share price performance, I am looking forward to all the January/February trading updates and the ongoing verification of my investment theses. In particular, I am mindful of the overweight position in AAZ and the extra risk that carries – perhaps I will be rewarded for that risk in 2021.

Portfolio Characteristics

Forecast dividend yield for 2021 is 4.12%.

With Average Quality 84, Average Value 38, Average Momentum 72 and Weighted Volatility 3.03, the portfolio maintains its status (if it were a single entity) as an Adventurous High Flyer.

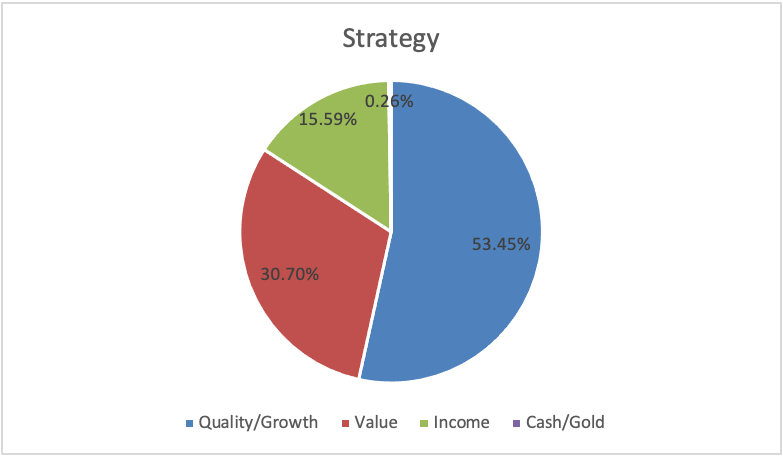

And this is how it breaks down by strategy:

Change of Benchmark

During the year I set up an ETF only portfolio on Wikifolio with the focus of achieving long-term growth from global equities. I am using a core-satellite approach and the portfolio has returned 18.7% (with a low point of -23.1%) since I set it up in February. I originally set it up as part of a conversation I was having with my adult kids about their own approach to investing and also what they should do with their inheritance when it eventually comes their way. I manage the Wikifolio semi-actively (review/rebalance quarterly) and am limited by the range of products available on the platform but nonetheless, I think it will prove a more relevant benchmark than Fundsmith (which I no longer own) and it will also give me the opportunity to benchmark my Wikifolio with Vanguard World (which is what it is trying to beat).

And I trust that the eagle-eyed amongst you will have noticed that I have managed to complete this entire review of 2020 without mentioning the title word once – just to prove it can be done!

On that note, it remains for me to wish all my readers and online investing buddies a very happy, healthy and prosperous 2021.

Cheers

Simon

Disclosure – At the time of writing I own shares in most of the shares mentioned in this article. A full list of current portfolio holdings can be viewed here