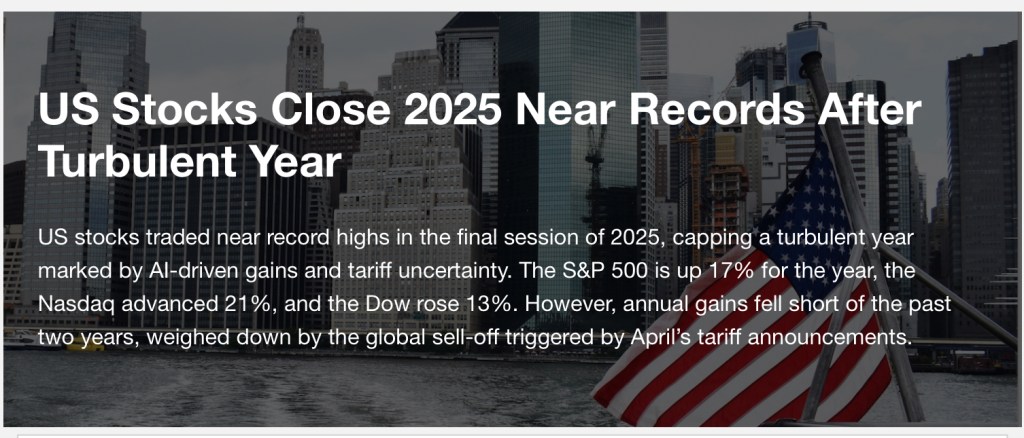

2025 was a turbulent year that worked out well in the end. It began with a new Trump presidency, escalated to Liberation Day tariffs, became moderated by TACO negotiation and ended near fearful all-time highs with the Fed reducing rates and loosening monetary policy.

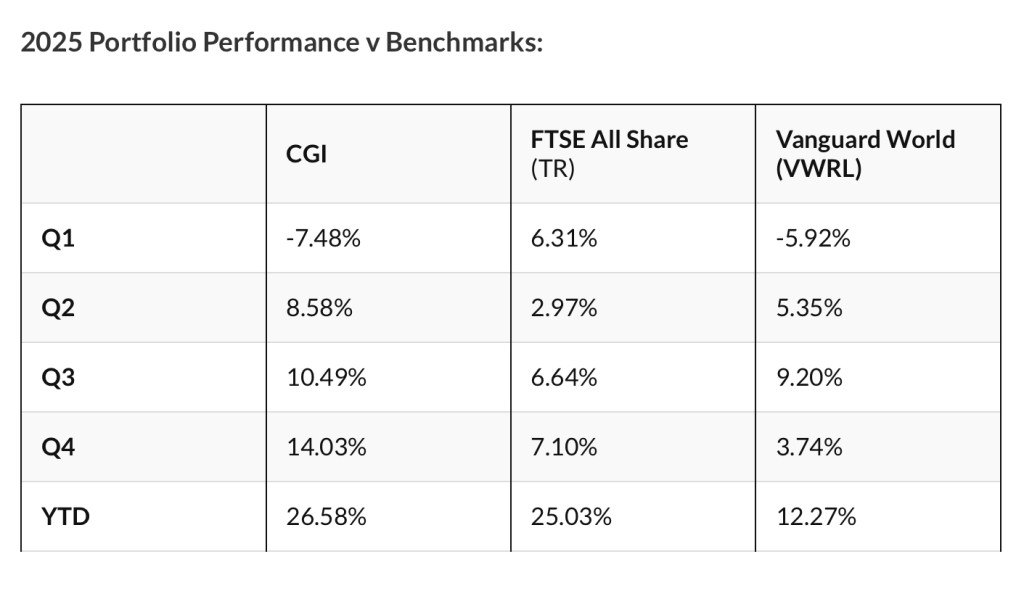

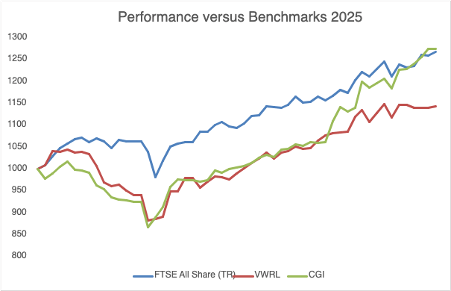

As for the UK, despite the worst efforts of the socialist government and the never-ending wait for a budget to fight its way past endless kite flying, the stock market actually did quite well, as did my own Compound Growth and Income (CGI) portfolio. Both outperformed the global index by some considerable margin.

Performance versus Benchmarks

In the end, a successful year returning 26.58% and a 10 year average annualised return that now sits at 22.16%

However, this relative success belies a year of extreme portfolio churn.

Portfolio Changes

Exits – Gamma Communications (GAMA), 4Imprint (FOUR), Bloomsbury Publishing (BMY), Mony Group (MONY), PayPoint (PAY), Warpaint (W7L), Property Franchise (TPFG), Fonix (FNX), Spectra Systems (SPSY), JP Morgan American (JAM), Henderson Far East Income (HFEL), CT Private Equity (CTPE), JP Morgan US Smaller Companies (JUSC).

In/Outs – Thor Explorations (THX), Fresnillo (FRES), Pan African Resources (PAF), Rolls-Royce (RR.), HG Capital Trust (HGT), Fidelity European (FEV), European Smaller Companies Trust (ESCT), Panthera Resources (PAT), Foresight Group (FSG), Smiths News (SNWS), Renewable Infrastructure (TRIG), Qualcomm (QCOM), Ark Innovations (ARCK), CT High Income (CHI), Telecom Plus (TEP).

New – Invesco Global Equity (IGET), Royal Mint Physical Gold (RMAP), iShares Gold Producers (SPGP), Golden Prospect Precious Metals (GPM), iShares Physical Silver (SSLN), Personal Group (PGH), TP Icap (TCAP), Polar Capital (POLR).

With that much churn, one would imagine it would have been quite difficult to make money EXCEPT…

Meddling Quotient

If I had done nothing with my start of year portfolio, I would have made 4.11% versus an actual return of 26.58%. This gives a positive meddling quotient of 22.47%. Carry on meddling Simon!

Dividends

Dividends for the year were 18% above forecast which was quite some feat given my switch to a number of non-yielding assets such as physical gold and silver.

Contributors and Detractors

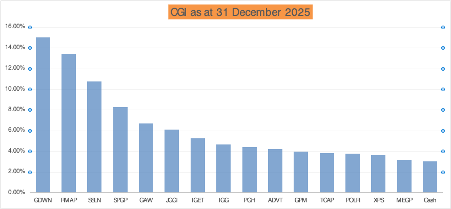

The standout performer of 2025 was Goodwin (GDWN) with a phenomenal 177% return, supported by solid contributions from Personal Group (PGH), Games Workshop (GAW) and IG Group (IGG).

Not shown in this graphic are the returns from investment trusts and ETFs where there were significant positive contributions from Royal Mint Physical Gold (RMAP) +40%, iShares Gold Producers (SPGP) +30%, iShares Physical Silver (SSLN) +75% and Golden Prospect Precious Metals +30% during the time I have held them.

As for the detractors, I managed to exit most of them before the damage was done. This damage would have been quite extreme if I had held onto them; Bloomsbury Publishing (BMY)-28%, Fonix (FNX) -23%, 4Imprint (FOUR) -20%, Gamma Communications (GAMA) -40%, PayPoint (PAY) -38%, Spectra Systems (SPSY) -33%, Warpaint (W7L) -60%, Wilmington -22%. Was this luck or judgement? Probably a bit of both with the main driver being to free up funds to invest in physical assets. I wrote some articles explaining my rationale for this as the year unfolded.

The Boy Who Cried Wolf in February

All that Glitters… in September

Gold and Goodwin in October

Picking through the Chaos in Macro Land

In no particular order…

President Trump will soon nominate a new Fed Chair to replace Jerome Powell in May 2026. This person is likely to be a dove, doing Trump’s bidding to drive interest rates down to 1% or below. This will almost certainly weaken the dollar which has already fallen by more than 10% this year in relation to other major currencies (the DXY index) and by around 65% when measured against gold. Whether these actions will help to make America great again by reshoring much of their manufacturing or alternatively, will lead to the fall of the dollar as the world’s reserve currency and perhaps even hyperinflation, remains to be seen.

Despite “agreements” being reached it is hard to argue against there being further bifurcation between East and West. The term Silk Curtain that I coined way back in April 2022 has not caught on but the bifurcation process has escalated with a potential monetary split; the BRICS ‘Unit’ is currently being trialled, BRICS countries and their neighbours are beginning to bypass the SWIFT system for international trade settlement along with export controls on strategic metals and rare earth minerals.

And I wonder who is going to buy the ~$9 Trillion of US debt that is due to expire in 2026 or indeed the $2-3 Trillion of additional debt that will be required to keep the lights on? With the East preferring to buy gold rather than US treasuries, will Western central banks be happy to buy a falling dollar or will that burden fall to the buyers of US Dollar Stable Coins? Or will President Trump pull a rabbit out of the hat and return to some form of gold backed currency?

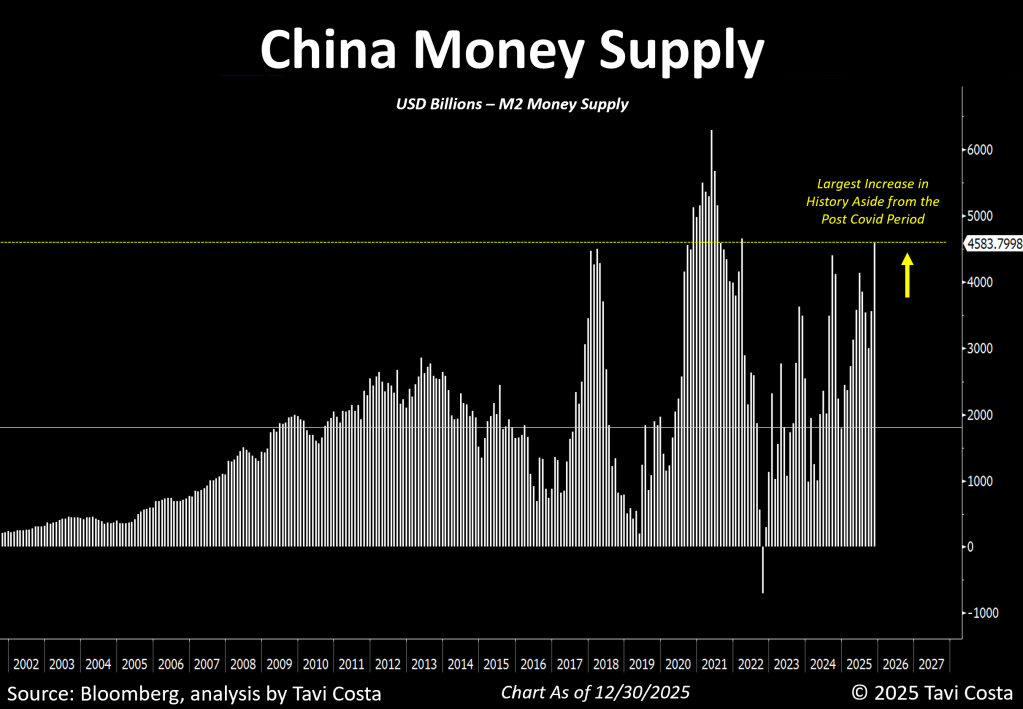

This might have gone under the radar but China has also had some pretty loose monetary policy in 2025.

The Yen carry trade (borrowing cheaply in Yen and investing in overseas assets) is unwinding now that Japanese interest rates are on the rise – currently over 2% for 10 year bonds.

Does AI present existential risk? Does AI present capex risk? Does AI present energy risk? Are AI stocks overvalued? Or does AI present genuine opportunity? I quite like using AI but what happens when the current Large Language Models (LLM) are superseded by Artificial General Intelligence (AGI)?

And what about actual war? Will there be a peaceful resolution between Russia and Ukraine or will it escalate into a European war? Will Middle Eastern conflicts escalate?

Will Central Bank Digital Currencies (CBDCs) gather pace in 2026? Are they a good thing? What will happen to individual freedoms?

Final Thoughts

With all this macro uncertainty (more so than usual, I would suggest), I think there are two ways I could play the potential chaos. Firstly, to increase diversification across assets and markets. Secondly, to consolidate around my best ideas and become more concentrated.

If I were to choose increased diversification, I would adopt something similar to the model portfolio I have just launched for The Compounding Machine.

If I were to consolidate, I would have to decide which holdings to cast aside and which ones and how many to focus on. Of my current 15 holdings, at least 6 would definitely make the cut – Games Workshop (GAW), Goodwin (GDWN), JP Morgan Global Growth & Income (JGGI), Invesco Global Equity Income (IGET), Royal Mint Physical Gold ETC (RMAP) and the iShares Gold Producers ETF (SPGP). I would probably also include Golden Prospect Precious Metals (GPM) and a new holding in Wheaton Precious Metals (WPM) which I am likely to pull the trigger on imminently. It would then be a case of which other holdings I would want to retain.

I shall continue to ponder the pros and cons and readers can tune into my January Share Watch article to see where I’ve landed. I also reserve the right, but not the obligation, to implement the third option of doing nothing at all!

In the meantime, it remains for me to wish all readers, subscribers and followers a happy, healthy and prosperous new year.

Best wishes

Simon (@BrilliantLeader)

Disclosure – At the time of writing, I own shares in the companies shown in the graphic below. My latest quarterly holdings disclosure can also be viewed here.