Looking back, the biggest concern the market seemed to have at the end of February was that AI might be disrupting software companies sooner than expected. And then March came along and President Trump, in conjunction with Israel, decided that now was a good time to attack Iran without having the foresight to secure the Strait of Hormuz first which Iran have subsequently taken control of and are now charging shipping tariffs for safe passage (with payment in Yuan or stablecoins). The market is now trying to work out how to price in an oil crisis, food shortages, supply chain disruption and the return of inflation vis-à-vis how long this Iran conflict will last.

The other event during March was a quarterly trading update from my largest holding, Goodwin (GDWN). The opening line was encouraging, “It is encouraging that the Group’s trading performance remains in line with expectations, as outlined in the October 2025 trading update.” For those not familiar, this equates to just over 100% increase in earnings. However, the trading update went downhill from there with the company warning of a lost tender for Easat (18m Euros) and more worryingly for Sellafield (£45m) along with negative vibes for the Jewellery division, Duvelco (expected delays to first commercial contracts), valves for LNG facilities (delayed thanks to disruption in the Middle East) and a potential reversal of the group’s enhanced dividend policy. A 50%+ decline in share price ensued. I think that is overdone even if the share price had got a little ahead of itself.

Suffice to say that both of these events represented a significant kick in the teeth for my portfolio which managed to retreat from a year-to-date high of +16.75% to end the quarter down 3.75%. A negative 20% swing was certainly not on my portfolio bingo card for March. The saving grace was that I top sliced some of my Goodwin shares at the end of January at £256 per share to fund some capital expenditures, including a lovely Caribbean holiday which is where my wife and I spent most of the past month. Switching off from the market noise (and not regularly checking the value of my portfolio) was much easier than it would have been under normal circumstances.

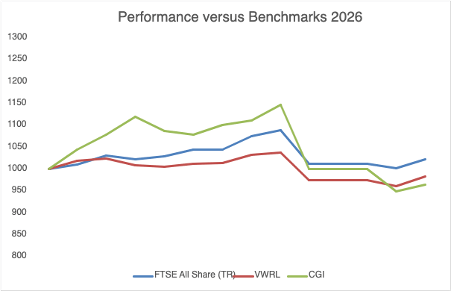

Performance versus Benchmarks

As signalled above, the portfolio went from a significant outperformance at the end of February to an underperformance by the end of the quarter.

Company News

Goodwin (GDWN) – Trading Update – As above.

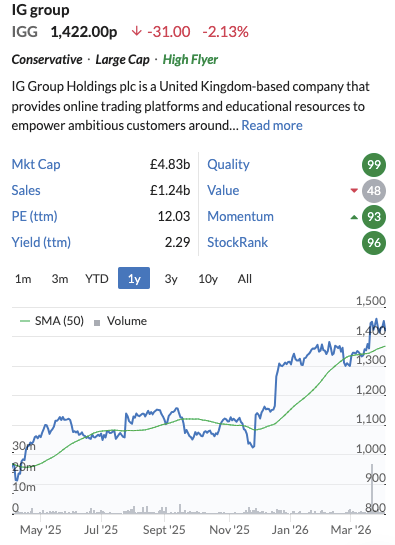

IG Group (IGG) – Full Year Results – Revenue increased 7%, EPS increased 5%, launch of a new share buyback programme of £125m and the announcement of a strategic review which will be published in the autumn, “The review will evaluate routes to maximise shareholder value, including, but not limited to, acquisitions to accelerate growth, IG’s domicile and listing venues to unlock capital and enhance strategic flexibility, and potential combinations of parts of the Group with other industry participants.” The market has responded positively and the shares remain good value in my opinion.

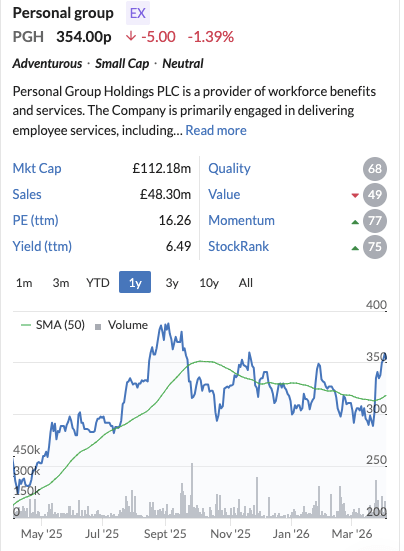

Personal Group (PGH) – Full Year Results – Revenue up 11%, EPS up 32% and Dividend up 41% (representing a 100% payout ratio). The market reacted positively to these results although the share price has still not reclaimed recent highs.

Dividends

Only two holdings paid a dividend in March, Games Workshop (GAW) and Gold Income Shares (GLDE) advancing the running total to 17% of my annual forecast.

Portfolio Changes

I exited the CT Managed Income Portfolio (CMPI) and the VanEck Gold Miners ETF (GDGB) during March, replacing them with a couple of extra high dividend payers (both of which are also potential value traps and/or higher risk products, so caveat emptor); Global X Super Dividend (SDIP) and JP Morgan Nasdaq100 Covered Calls (JEQP). While I remain a gold bull, gold miners have a dual headwind of lower gold prices and higher oil prices, so GDGB reduces my exposure to this industry while CMPI was really just an income placeholder. Adding some higher yield products is mainly a case of battening down the hatches while current macro and geopolitical factors play out.

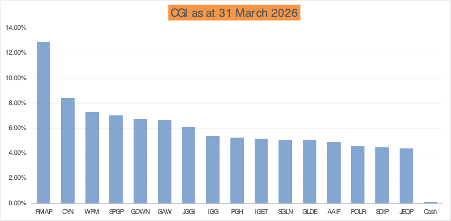

These changes leave me holding 10 funds (Investment Trusts and ETFs) and 6 individual companies, generating a natural portfolio yield of around 4.5%. The current portfolio holdings/weightings are shown in the graphic below.

Outlook

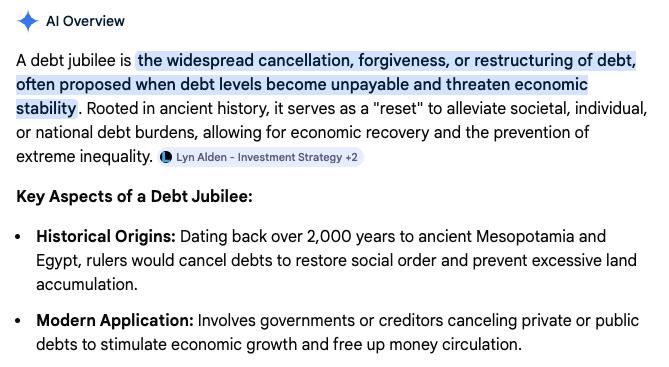

Aside from the human tragedy, this Iranian/Middle East conflict is a further step in the bifurcation of the world between East and West or judging by Trump’s rhetoric, perhaps it is the U.S. and the RoW. I can’t help thinking though that this is a smokescreen for what is really happening under the surface, be that an AI race, energy security/dominance or some form of monetary reset. The move by Iran to allow passage for a tariff payable in Yuan or stablecoins competes with the petrodollar and bypasses the SWIFT system. And with the U.S. debt heading towards $40 trillion one wonders whether a monetary reset will be a debt jubilee in all but name.

Gold

I continue to hold gold, primarily to try and insulate my portfolio from the effects of monetary reset and dollar debasement. It also provides some protection against inflation/stagflation. I currently have 25% allocated to physical gold and a further 20% in mining/streaming companies.

Closing Thoughts

Whatever is coming down the tracks, it ain’t gonna be pretty! Energy and perhaps food shortages, supply chain disruption, recession/inflation/stagflation, AI disruption – take your pick and plan accordingly. And remember, this mayhem will eventually pass and the way forward will become clearer.