The main market event in February has been the decline in software and professional service companies amid concern that their business models will be disrupted by Artificial Intelligence (AI), perhaps sooner than had previously been anticipated. Moats might weaken, margins decline and white-collar unemployment increase, perhaps rapidly. Companies that were previously regarded as high-quality compounders are now derating to reflect these risks, even though said risks have been present in the background for a while now.

Perhaps The 2028 Global Intelligence Crisis by Citrini Research has helped to focus minds. It is a thought-provoking scenario even if the evidence and timeframes are somewhat speculative and subjective.

Personally, I have been thinking about the impact of AI for a while now and concluded that it is going to be hellishly difficult to pick the winners and losers with any degree of certainty. Even the so called hyper-scalers have been running up large debts (some might say placing large bets) on capital expenditure in the race to dominate the space. This uncertainty is one of the reasons (alongside a potential monetary reset and continued geopolitical strife) that I have reduced my direct equity holdings significantly. Instead, I have been increasing my exposure to gold and other commodity producers, mainly via funds.

The one thing that seems certain is that digitalisation and electrification are driving the need for a wide range of commodities such as silver, copper, lithium, rare earths and energy. Overall, metals and mining exposure is now around 50% of my portfolio from seven holdings.

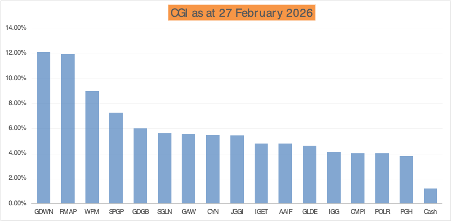

Royal Mint Physical Gold (RMAP) ~12%

Wheaton Precious Metals (WPM) ~9%

Ishares Gold Producers (SPGP) ~7%

VanEck Gold Miners (GDGB) ~6%

iShares Physical Gold (SGLN) ~5.5%

CQS Natural Resources (CYN) ~5.5%

Income Shares Gold (GLDE) ~5%

Perhaps I am being artificially intelligent but it seems like quite a simple and elegant solution to the AI dilemma, bifurcation of trade and geopolitical strife. My very own Mag 7.

For the record, the remainder of my portfolio is spread across Global Equities (JGGI and IGET), Asian Equities (AAIF), Goodwin (Diversified Industrial Engineering), Games Workshop (Toy Soldiers), UK Equities (CMPI) and three financial stocks (IGG, POLR, PGH). The latter names mentioned might or might not survive the brutality of my culling as the future unfolds but for now, the dividend income is useful.

My apologies for the brevity of this month’s update but sometimes, when you have little to say, it is best to say little. Normal service will be resumed next month with my quarterly review where hopefully I will be reporting on a positive quarter, given that the running total is +15% YTD – which is brilliant but also bonkers!

Disclosure – Current portfolio holdings and weightings are listed in the graphic below.